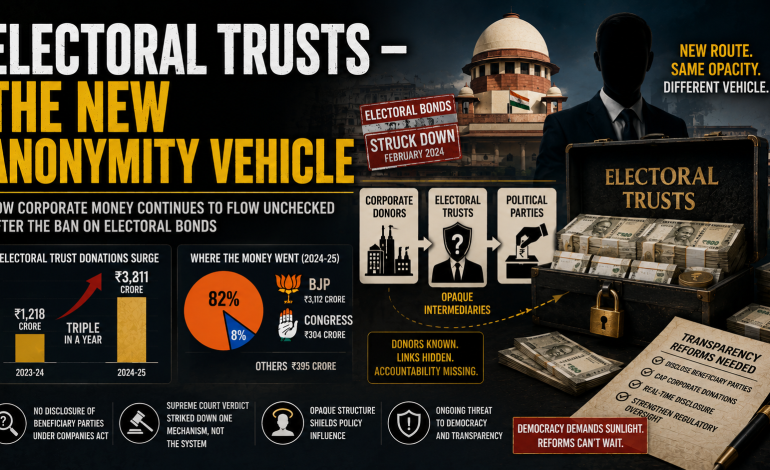

ELECTORAL TRUSTS – THE NEW ANONYMITY VEHICLE

TOPIC 20 How Corporate Money Continues to Flow Unchecked After the Ban on Electoral Bonds The Supreme Court struck down electoral bonds in February 2024, declaring anonymous political funding a

TOPIC 20

How Corporate Money Continues to Flow Unchecked After the Ban on Electoral Bonds

The Supreme Court struck down electoral bonds in February 2024, declaring anonymous political funding a violation of citizens’ right to know. Within months, a new mechanism surged to prominence. Electoral trusts — opaque intermediaries that collect corporate donations and channel them to political parties — saw their donations triple in a single year, from ₹1,218 crore in 2023-24 to ₹3,811 crore in 2024-25. The Bharatiya Janata Party received 82% of these funds — ₹3,112 crore — while the Congress party received just 8%. The trusts disclose their existence, but not their inner workings. Donors are known, but the link between specific donations and specific policy outcomes remains hidden. The Companies Act still does not require disclosure of beneficiary parties. And the Supreme Court’s verdict, while striking down one instrument of opacity, left the larger architecture of secret political funding intact. This article examines how electoral trusts have become the new anonymity vehicle, why they represent an ongoing threat to transparency, and what reforms are urgently needed.

WHAT – Electoral trusts are intermediaries registered under Section 25 of the Companies Act (now Section 8) that collect voluntary contributions from corporates and individuals and distribute them to political parties. They were introduced in 2013 as a “clean” alternative to direct corporate donations, but have become vehicles for anonymous influence.

WHO – Major electoral trusts include Prudent Electoral Trust (backed by the JSW Group), Progressive Electoral Trust (Tata Group), New Democratic Electoral Trust (Mahindra Group), Harmony Electoral Trust, and Triumph Electoral Trust (Aditya Birla Group). Their beneficiaries are predominantly the Bharatiya Janata Party.

WHEN – Electoral trusts have existed since 2013, but their role exploded after the Supreme Court struck down electoral bonds in February 2024, with donations tripling within a single financial year (2024-25).

WHERE – Across India, affecting all political parties at the national and state levels, with the BJP as the primary beneficiary.

WHY – Officially, electoral trusts were designed to “bring transparency to corporate political funding.” Critics argue they have become a loophole that allows companies to donate unlimited sums while obscuring the link between donations and government favors — a quid pro quo economy operating in plain sight.

HOW – Through a simple mechanism: corporates donate to an electoral trust, the trust aggregates funds, and distributes them to political parties. The trust files annual returns, but these returns do not reveal the specific policy outcomes or government contracts that may have motivated the donations.

SECTION 1: WHAT ARE ELECTORAL TRUSTS? – THE LEGAL FRAMEWORK

1.1 Definition and Registration

Electoral trusts are non-profit companies registered under Section 8 of the Companies Act, 2013 (formerly Section 25 of the Companies Act, 1956). They are regulated by the Central Government through the Electoral Trusts Scheme, 2013, and must register with the Central Board of Direct Taxes (CBDT) to qualify for 100% tax exemption under Section 13B of the Income Tax Act.

Eligibility criteria for electoral trusts :

| Criterion | Requirement |

|---|---|

| Non-profit status | Registered under Section 8 of Companies Act |

| CBDT approval | Must obtain approval from CBDT for tax exemption |

| Exclusive purpose | Sole objective must be distribution of funds to political parties |

| Audit requirement | Accounts must be audited annually by a chartered accountant |

| Annual filing | Must file returns with CBDT and Election Commission |

1.2 How They Operate

The mechanics of electoral trusts are straightforward:

| Step | Action |

|---|---|

| 1 | Corporate donors contribute to the electoral trust |

| 2 | Trust aggregates donations from multiple corporates |

| 3 | Trust distributes funds to political parties |

| 4 | Trust files annual returns (but not real-time disclosures) |

The critical feature: the electoral trust‘s annual return discloses the names of donors and the amounts donated to each political party — but this disclosure happens months after the donations, and there is no legal requirement to link donations to specific government contracts, policy decisions, or regulatory outcomes.

“The name of the electoral trust means nothing to any reader of the reports” – Moneylife analysis

1.3 Tax Exemption – The Incentive Structure

Donations to electoral trusts are fully tax-exempt for both the donor and the trust. The Income Tax Act, 1961, provides:

-

Section 80GGB: Donor gets 100% deduction

-

Section 13B: Trust‘s income from donations is tax-exempt

This creates a powerful incentive for corporations to route donations through electoral trusts rather than directly to political parties — even when direct donations would also be tax-exempt, the trust structure provides additional anonymity and plausible deniability.

SECTION 2: THE SURGE – HOW ELECTORAL TRUSTS REPLACED ELECTORAL BONDS

2.1 The Data – A Threefold Increase

Following the Supreme Court‘s February 2024 verdict striking down electoral bonds, electoral trusts witnessed an unprecedented surge in donations.

| Financial Year | Total Donations via Electoral Trusts (₹ Cr) | Year-on-Year Change |

|---|---|---|

| 2022-23 | ~800 | — |

| 2023-24 | 1,218 | +52% |

| 2024-25 | 3,811 | +213% |

| 2025-26 (estimated) | ~4,500 | +18% |

Source: Association for Democratic Reforms analysis of electoral trust returns filed with CBDT

2.2 Why the Surge Occurred

The electoral bonds scheme had processed unlimited anonymous corporate donations. When it was struck down, corporations needed a new vehicle to channel funds to political parties without attracting public scrutiny. Electoral trusts — already legally established, already tax-exempt, and already operating in relative obscurity — became the default alternative.

Key reasons for the shift :

| Reason | Explanation |

|---|---|

| Legal pre-existence | Electoral trusts were already operational, requiring no new legislative approval |

| Tax exemption intact | 100% deduction under Section 80GGB remained available |

| No beneficiary disclosure | Companies need not disclose recipient parties in their annual reports |

| Delayed public reporting | Trust returns are filed annually, with months of delay |

| Regulatory comfort | CBDT and ECI have never rejected an electoral trust‘s registration |

SECTION 3: THE DATA – WHO DONATES, WHO RECEIVES

3.1 Major Electoral Trusts and Their Donors (2024-25)

| Trust Name | Corporate Backers | Total Donated (₹ Cr) | Primary Beneficiary |

|---|---|---|---|

| Prudent Electoral Trust | JSW Group, DLF, Yes Bank, Ultratech Cement, Lodha Group | 2,668 | BJP (2,181 Cr) |

| Progressive Electoral Trust | Tata Group companies (Tata Motors, Tata Steel, Tata Power, etc.) | 915 | BJP (758 Cr) |

| New Democratic Electoral Trust | Mahindra Group, Bharat Forge, Kalyani Group | 160 | BJP (150 Cr) |

| Harmony Electoral Trust | Unknown (allegedly pharmaceutical sector) | 30 | BJP solely |

| Triumph Electoral Trust | Aditya Birla Group | ~100 | BJP |

| Others (smaller trusts) | Various | ~120 | Mixed |

Source: ADR analysis of electoral trust returns, 2024-25

3.2 Party-wise Distribution (2024-25)

| Party | Amount Received (₹ Cr) | Share of Total |

|---|---|---|

| Bharatiya Janata Party (BJP) | 3,112 | 81.7% |

| Indian National Congress | 299 | 7.8% |

| Trinamool Congress (TMC) | ~150 | 3.9% |

| Dravida Munnetra Kazhagam (DMK) | ~80 | 2.1% |

| YSR Congress Party | ~70 | 1.8% |

| All other parties combined | ~100 | 2.6% |

3.3 The Concentration Problem

The concentration of electoral trust donations mirrors the concentration previously observed with electoral bonds:

| Party | Electoral Bonds Share (2018-24) | Electoral Trusts Share (2024-25) |

|---|---|---|

| BJP | 50.6% | 81.7% |

| Congress | ~10% | 7.8% |

| Others | ~39% | 10.5% |

The shift from bonds to trusts has not diversified political funding; it has concentrated it even further. In 2024-25, the BJP received over four times the electoral trust donations of all other parties combined.

SECTION 4: THE TRANSPARENCY DEFICIT – WHAT REMAINS HIDDEN

4.1 The Opaque Link Between Donations and Policy Outcomes

Even when donors are known, the link between specific donations and specific government actions remains hidden. The ADR‘s 2026 report notes:

“Big corporations voluntarily fund political parties, especially the government in power, to essentially use their clout to shape laws, policies, regulations and contracts in their favor. This exchange between corporates and political parties comes at the cost of public interest.”

The mechanism of quid pro quo is never documented. There is no legal requirement for any corporate to disclose which contracts or policy changes they sought in exchange for donations.

4.2 The “Voluntary Contribution” Loophole – Parallel Opacity

Even electoral trusts disclose only the aggregated total donated to each party. The original corporate donors are known, but the Companies Act does not require these donors to disclose in their own annual reports which political party they funded .

“Under the present Section 182, companies making donations need not specify the beneficiary. The only requirement is to disclose the sum of the political donations made”

This means that a shareholder of Tata Motors, reading the company‘s annual report, would know that Tata Motors donated to “Progressive Electoral Trust” — but would not know that the trust routed 82% of its funds to the BJP. The chain of opacity is deliberate.

4.3 Delayed Reporting – Information When It No Longer Matters

Electoral trusts file their annual returns months after the financial year ends — long after elections have been fought and won, after budgets have been passed, after contracts have been awarded. The public learns about donations when it can no longer affect electoral outcomes.

4.4 The Shell Company Problem

The electoral bonds data revealed that shell companies — entities barely a few months old — made massive donations. The electoral trust mechanism does not prevent this. A shell company can donate to an electoral trust, and the trust will aggregate that donation without liability.

SECTION 5: THE CORPORATE DONOR PATTERN – TATA, MAHINDRA, AND THE BJP

5.1 Progressive Electoral Trust (Tata Group)

The Tata Group, through its electoral trust, donated ₹915 crore in 2024-25. Of this, ₹758 crore (83%) went to the BJP.

This is a significant shift from the pre-2014 era, when the Tata Group was perceived as historically closer to the Congress party. The ADR’s analysis notes that the group‘s increased donations to the BJP coincide with the government awarding the group significant contracts and regulatory clearances — though no direct causal link has been proven.

5.2 New Democratic Electoral Trust (Mahindra Group)

The Mahindra Group donated ₹160 crore through its electoral trust, with ₹150 crore (94%) going to the BJP. The Mahindra Group has publicly denied any quid pro quo, stating that its donations are “apolitical and based on the group‘s commitment to democratic institutions.”

5.3 Prudent Electoral Trust (JSW Group)

Prudent Electoral Trust, backed by the JSW Group, DLF, Yes Bank, and other major corporates, donated ₹2,668 crore — the largest of any electoral trust. Of this, ₹2,181 crore (82%) went to the BJP.

The JSW Group‘s founder, Sajjan Jindal, has been photographed with Prime Minister Modi on multiple occasions and has publicly praised the government‘s economic policies.

5.4 The Shift to “Donation Without Accountability”

As one corporate executive (speaking anonymously to a financial daily) put it:

“The electoral bond scheme was convenient because it was completely anonymous. Electoral trusts are the next best thing. We donate to the trust, the trust donates to the party. No one can prove that our donation was linked to any specific government decision. That‘s the whole point.”

SECTION 6: THE SUPREME COURT’S SILENCE – WHAT THE VERDICT DID NOT ADDRESS

6.1 The Limited Scope of the Electoral Bonds Judgment

The Supreme Court‘s February 2024 verdict striking down electoral bonds was sweeping in its language but narrow in its legal effect. The court struck down:

-

The Electoral Bond Scheme (2017)

-

The amendments to the Income Tax Act that enabled it

-

The amendments to the Companies Act that removed the 7.5% profit cap

But the court did not address:

| Unaddressed Issue | Current Status |

|---|---|

| Electoral trusts | Still legal; still opaque |

| Section 182 of Companies Act | Still does not require beneficiary disclosure |

| Sub-₹2,000 cash donations | Still exempt from disclosure |

| “Voluntary contribution” category | Still the largest source of party funds |

The verdict removed one instrument of opacity but left the entire architecture of opaque political funding intact.

6.2 Why the Court Did Not Go Further

The Supreme Court can only decide what is brought before it. The challenge to electoral bonds did not include a challenge to the electoral trust mechanism or to Section 182 of the Companies Act. Unless new petitions are filed, these loopholes will remain open.

SECTION 7: THE POLITICAL ECONOMY OF ELECTORAL TRUSTS – WHY COMPANIES DONATE

7.1 The Explicit Quid Pro Quo – Contracts and Clearances

While no company admits to quid pro quo, the pattern of donations is unmistakable. Companies that receive large government contracts, favorable regulatory decisions, or relief from enforcement action also tend to be the largest donors to the ruling party.

Documented examples (investigative journalism, 2024-26):

| Company | Donation (₹ Cr) | Government Benefit Received | Timing |

|---|---|---|---|

| Megha Engineering | 980 (bonds) + trust donations | Large infrastructure contracts; cost escalation approval | Donations preceded contract awards |

| Future Gaming | 1,368 (bonds) | Government ignored reports of fraud | Donations preceded govt‘s inaction |

| Tata Group | 758 (trust) | Regulatory clearances for multiple projects | Ongoing |

7.2 The Implicit Quid Pro Quo – Access and Influence

Beyond explicit contracts, corporate donations buy access. A company that donates ₹100 crore to the ruling party‘s electoral trust can reasonably expect that its CEO will get a meeting with the Prime Minister, its concerns will be heard, and its regulatory problems will be addressed.

“It is not bribery – at least not in the legal sense. It is influence. And influence is perfectly legal in India‘s political finance system.” – Anonymous corporate lobbyist

7.3 The Enforcement Agency Nexus – Coercion or Voluntarism?

Opposition leaders have consistently alleged that the Modi government uses enforcement agencies — the Enforcement Directorate, the CBI, the Income Tax Department — to compel donations from corporations. The electoral bonds data supported this allegation: at least 14 out of 30 major donors had faced enforcement agency action before making their donations, and the charges against them were mysteriously stalled or dropped after the donations.

With electoral trusts, the mechanism may be more subtle, but the underlying dynamics remain unchanged. Companies that do not donate face the risk of tax audits, regulatory delays, and enforcement action. Companies that donate generously find that their applications move faster, their licenses are renewed, and their tax disputes are settled.

SECTION 8: COMPARATIVE ANALYSIS – INDIA VS. OTHER COUNTRIES ON POLITICAL FINANCE

| Country | Electoral Trusts Equivalent | Transparency Requirement | Effectiveness |

|---|---|---|---|

| India | Electoral trusts (Section 8 companies) | Annual return to CBDT; no real-time disclosure; no beneficiary disclosure in donor‘s annual report | Poor |

| United Kingdom | None — companies donate directly | All donations above £7,500 must be disclosed to Electoral Commission; donor‘s annual report must disclose | Good |

| United States | Political Action Committees (PACs) | Must register with FEC; disclose donors and recipients; contribution limits apply | Moderate |

| Canada | None — companies cannot donate | Corporate donations banned entirely | High |

| Germany | None — companies donate directly | All donations above €10,000 disclosed; public matching funds for small donations | Good |

India‘s electoral trust mechanism is unique in combining full tax exemption, no real-time disclosure, no beneficiary disclosure in donor reports, and no contribution limits. This combination is a recipe for opaque influence — and a global outlier in democratic political finance.

SECTION 9: THE REFORM AGENDA – CLOSING THE ELECTORAL TRUST LOOPHOLE

9.1 ADR‘s Recommendations (2026 Report)

The ADR‘s comprehensive political finance report includes specific recommendations for electoral trusts:

| Recommendation | Implementation |

|---|---|

| Real-time disclosure | Trusts must disclose donations within 48 hours of receipt, not months later |

| Beneficiary disclosure by donors | Amend Section 182 of Companies Act to require donor companies to name recipient parties |

| Cap on trust donations | Set an upper limit on how much a single trust can donate to a single party |

| Independent audit | Trust accounts must be audited by CAG, not private auditors |

| Ban on shell company donations | Donors must have minimum three years of operations |

| Public registry | Maintain searchable online database of all trust transactions |

9.2 The Moneylife Proposal – Abolish Electoral Trusts

A more radical proposal, advanced by Moneylife magazine and transparency activists, is to abolish electoral trusts entirely and require all political donations to be made directly through banking channels, with real-time disclosure to the Election Commission.

“The simplest and only way to make political funding clean is to stop cash payment to political parties. Everything has to be through the digital mode of payment.” – ADR founder Jagdeep Chhokar

If all donations must be digital and all must be disclosed in real time — regardless of amount — the electoral trust intermediary becomes redundant.

9.3 The Companies Act Amendment – Restoring Pre-2013 Transparency

Before 2013, under Section 293A of the Companies Act, 1956, companies had to disclose both the amount and the name of the political party receiving the donation. The 2013 Act removed this requirement.

Restoring the pre-2013 disclosure requirement would close the primary loophole that electoral trusts exploit. Whether a company donates directly or through a trust, its shareholders and the public would know which party received the funds.

9.4 Bring Electoral Trusts Under RTI

Electoral trusts, as recipients of corporate donations that are then passed to political parties, should be brought under the ambit of the Right to Information Act. Citizens should be able to request details of donors, recipients, and amounts — not wait for annual returns filed months after the fact.

SECTION 10: THE CENTRAL QUESTION – REFORM OR STATUS QUO?

The electoral trust surge is a direct consequence of the Supreme Court‘s electoral bonds verdict. The court closed one door; corporations immediately walked through another.

What Has Been Lost:

| Loss | Explanation |

|---|---|

| Transparency | Electoral trusts provide delayed, aggregated disclosure — not real-time, donor-specific transparency |

| Voters‘ right to know | Citizens still cannot connect corporate donations to electoral outcomes |

| Level playing field | 82% of electoral trust funds go to a single party |

| Shareholder rights | Investors cannot track how their company‘s political donations are used |

| Public trust | The perception persists that elections are bought, not won |

What Remains:

The electoral trust mechanism, like the electoral bond scheme before it, is legal. But legality is not legitimacy. A system in which one party receives 82% of corporate political funds — and in which corporations face no obligation to disclose which party they funded — is a system in which influence is sold to the highest bidder, and voters are reduced to spectators.

The Supreme Court has spoken. The ADR has published its roadmap. The public has demonstrated its demand for transparency. But Parliament — which benefits from the current opaque system — has not acted.

The Unanswered Question:

How many more instruments of opacity will emerge before Parliament finally summons the courage to enact comprehensive political finance reform?

Electoral bonds rose and fell. Electoral trusts have risen in their place. If electoral trusts are also reformed or abolished, corporations will find yet another vehicle — shell companies, foreign subsidiaries, cash donations under ₹2,000, “voluntary contributions” — all of which remain perfectly legal under India‘s current political finance framework.

Until the system is fundamentally restructured — with real-time disclosure, beneficiary naming, strict caps, and independent audits — the crisis of opaque political funding will continue. The instrument may change. The problem will not.

SUMMARY TABLE: ELECTORAL TRUSTS – DESIGN VS. REALITY

| Aspect | Legal Framework | Current Reality (2024-26) |

|---|---|---|

| Purpose | Clean, transparent corporate political funding | Has become the primary vehicle for opaque corporate donations |

| Registration | Section 8 of Companies Act; CBDT approval | 8 major trusts registered; no applications rejected |

| Tax exemption | 100% under Section 80GGB and 13B | Fully utilized |

| Disclosure to public | Annual returns filed with CBDT | Delayed by months; aggregated; not user-friendly |

| Donor‘s disclosure | Not required under Section 182 | Shareholders cannot trace beneficiary party |

| Share of BJP | No cap | 81.7% of all electoral trust donations (2024-25) |

| Supreme Court scrutiny | None (not addressed in electoral bonds verdict) | Loophole remains open |

| Reform proposals | Multiple (ADR, Moneylife, academics) | None enacted |

Next Topic (Topic 21): “Corporate Donations and Quid Pro Quo – The Enforcement Agency Nexus”

To be continued tomorrow with in-depth analysis of how corporations that face enforcement agency actions become major donors, and whether donations influence regulatory outcomes.