TAXATION ON SAVINGS AND MIDDLE-CLASS ANXIETY

TAXATION ON SAVINGS AND MIDDLE-CLASS ANXIETY How Taxation Policies Affect Small Investors and Households On February 1, 2026, Finance Minister Nirmala Sitharaman stood before Parliament to present the Union Budget

TAXATION ON SAVINGS AND MIDDLE-CLASS ANXIETY

How Taxation Policies Affect Small Investors and Households

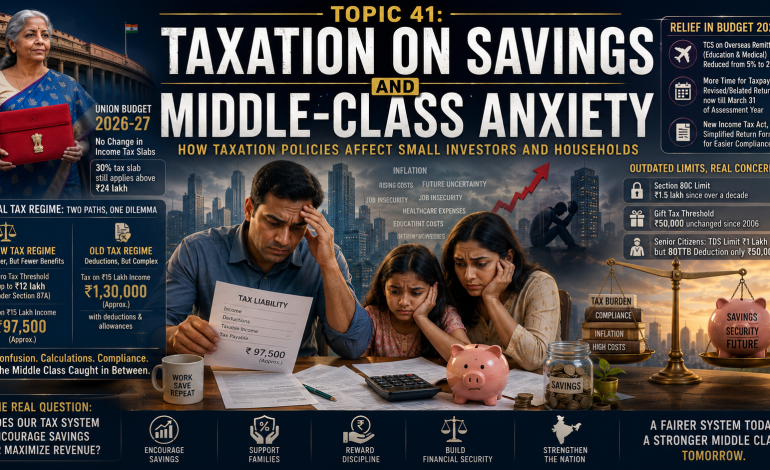

On February 1, 2026, Finance Minister Nirmala Sitharaman stood before Parliament to present the Union Budget for financial year 2026-27. For weeks beforehand, the middle class had been speculating, hoping, and worrying. Would the government raise the 30 percent tax slab threshold from ₹24 lakh to ₹35 lakh? Would standard deduction be increased? Would health insurance and home loan deductions finally be allowed under the new tax regime? As the speech unfolded, the answer became clear: income tax slabs would remain unchanged. The 30 percent rate would still apply to incomes above ₹24 lakh. The new tax regime’s zero-tax threshold would stay at ₹12 lakh through the Section 87A rebate.

For the salaried employee with a ₹15 lakh package, the math was familiar and frustrating. Under the new regime, tax liability stood at approximately ₹97,500. Under the old regime, with its maze of deductions, the liability was around ₹1.30 lakh—unless the taxpayer could access allowances like HRA and children’s education benefits. The gap between the two regimes was narrowing, but confusion persisted. Many middle-class families found themselves trapped between two imperfect systems: the new regime’s simplicity with its denial of popular deductions, and the old regime’s tax-saving opportunities with its cumbersome compliance requirements.

Yet the 2026 Budget was not without relief for the anxious middle class. The government introduced a series of compliance simplifications that, while less dramatic than headline tax cuts, addressed the everyday frustrations of small taxpayers. TCS rates on overseas remittances for education and medical treatment were reduced from 5 percent to 2 percent, easing the cash flow burden on families sending children abroad for studies. The window for filing revised or belated returns was extended to March 31 of the assessment year, giving taxpayers more time to correct mistakes. The rollout of the new Income Tax Act, 2025, promised simplified return forms that ordinary taxpayers could file without professional assistance.

But lurking beneath these incremental changes was a deeper anxiety—one that no single budget could resolve. The old tax regime’s Section 80C limit of ₹1.5 lakh had remained unchanged for over a decade, even as inflation eroded the real value of investments in PPF, ELSS, and life insurance. The threshold for taxing gifts under Section 56(2)(x) had not been revised since 2006, when ₹50,000 was a substantial sum. Senior citizens faced a mismatch between the enhanced TDS threshold on interest income (₹1 lakh) and the unchanged deduction limit under Section 80TTB (₹50,000). The middle class was not just paying taxes—it was navigating a system that had failed to keep pace with economic reality.

This article examines how taxation policies affect small investors and middle-class households in India. It explores the structural features of the dual tax regime, the specific anxieties that drive middle-class financial behavior, the impact of recent Budget changes, and the fundamental question of whether India’s tax system is designed to encourage savings or to maximize revenue at the expense of household financial security.

WHAT – Taxation on savings refers to the various ways in which income tax laws affect how middle-class households save, invest, and plan for long-term financial goals. This includes taxes on income from savings (interest, dividends, capital gains), deductions available for certain investments (Section 80C, 80D, home loan interest), the choice between old and new tax regimes, and compliance burdens such as TDS/TCS requirements and return filing obligations.

WHO – Individual taxpayers, particularly salaried employees in the ₹5 lakh to ₹25 lakh annual income bracket, form the core of the “middle class” affected by these policies. Small investors in instruments like PPF, EPF, mutual funds (ELSS), life insurance, and National Savings Certificates are directly impacted. Financial advisors, tax consultants, industry bodies (PHDCCI, Grant Thornton), and the Income Tax Department are the key institutional actors. The Finance Ministry and the Prime Minister’s Office set policy direction through the annual Budget.

WHEN – The current tax framework operates under the old regime (with deductions) and the new regime (lower rates, fewer deductions) introduced in 2020 and significantly modified in 2023 and 2025. The Budget 2026 (presented February 1, 2026) introduced further changes effective from April 1, 2026 (Assessment Year 2026-27). The Draft Income-tax Rules, 2026 (released February 7, 2026) proposed enhanced limits for various allowances and perquisites.

WHERE – Across India, with particular intensity in metropolitan cities like Mumbai, Delhi, Bengaluru, Chennai, Hyderabad, Pune, and Ahmedabad, where housing costs (and thus HRA claims) are highest. However, middle-class tax anxiety is a national phenomenon, affecting households in Tier-2 and Tier-3 cities as well.

WHY – The middle class feels acute tax anxiety because of several converging pressures: stagnant real wage growth in many sectors, rising costs of housing, healthcare, and education, the need to save for retirement in the absence of robust social security, and the complexity of a tax system that requires active planning to minimize liability. Unlike high-net-worth individuals who can afford professional tax advisors, middle-class households must navigate this complexity themselves or rely on limited employer support.

HOW – Through the dual tax regime structure, where taxpayers can choose between the old regime (higher rates but deductions under Sections 80C, 80D, 80E, HRA, LTA, home loan interest) and the new regime (lower rates but almost no deductions except standard deduction and employer NPS contribution). Tax liability is computed based on income slabs, with rebate under Section 87A eliminating tax for incomes up to ₹12 lakh under the new regime. TDS/TCS mechanisms collect tax at source, while advance tax provisions require quarterly payments for those with substantial non-salary income. Capital gains tax applies to investment returns, with different rates for short-term and long-term holdings.

SECTION 1: THE MIDDLE-CLASS ANXIETY — WHY SAVINGS TAXATION MATTERS

The Definitional Problem

Who is the “middle class” in Indian tax discourse? The term is notoriously slippery, used by politicians and commentators alike to evoke a constituency that is neither rich enough to ignore taxes nor poor enough to be fully exempt. For practical purposes, the middle-class taxpayer in India is the salaried individual earning between ₹5 lakh and ₹25 lakh annually—above the basic exemption limit (₹2.5 lakh under old regime, effectively ₹4 lakh under new regime) but below the top surcharge brackets.

This segment is distinctive in three ways. First, its income is predominantly from salary, meaning taxes are deducted at source (TDS) before the taxpayer ever sees the money—creating a psychological sense of loss that business owners, who pay advance tax on their own terms, do not experience. Second, its savings are not optional but essential: without retirement planning through EPF/PPF, health insurance, and children’s education funds, the middle class faces financial precarity in old age. Third, it lacks the resources for sophisticated tax avoidance strategies available to the wealthy, relying instead on the standard deductions and exemptions built into the tax code.

The Savings-Incentive Disconnect

The original logic of tax deductions for savings, embodied in Section 80C and its predecessors, was straightforward: the government would forgo revenue today to encourage households to save for retirement, housing, and emergencies. A rupee saved in PPF was a rupee not spent on consumption—and, theoretically, a rupee channeled into long-term national investment.

But this logic has frayed. The ₹1.5 lakh limit under Section 80C has remained unchanged since 2014, even as nominal incomes have grown significantly. A taxpayer earning ₹10 lakh in 2014 could save 15 percent of their income tax-free. A taxpayer earning ₹20 lakh in 2026 can save only 7.5 percent. The incentive to save has been halved by bracket creep—the failure to adjust deduction limits for inflation.

The Compliance Burden

Beyond the arithmetic of tax liability lies the psychological weight of compliance. The Indian tax system is notoriously complex, with separate regimes, multiple deductions subject to different conditions, and annual changes that require constant relearning. A 2026 survey cited by Grant Thornton indicated that “ease of compliance is now as important as tax savings” for many middle-class taxpayers.

The salaried employee must track HRA eligibility, claim LTA within strict rules, maintain health insurance premium receipts, ensure that 80C investments are made before March 31, and file returns by July 31 (extended for non-audit cases to August 31 under Budget 2026). Any mistake triggers notices from the Income Tax Department—often automated, often for minor mismatches between AIS data and return filings. The fear of notices, not the tax liability itself, drives much middle-class anxiety.

SECTION 2: THE DUAL REGIME DILEMMA — CHOICE AS BURDEN

Structure of the Two Regimes

India’s dual tax regime, introduced in 2020 and significantly modified in 2023 and 2025, presents taxpayers with a choice between two fundamentally different approaches to taxation.

Old Tax Regime (with deductions/exemptions):

| Total Income (₹) | Tax Rate |

|---|---|

| 0 – 2,50,000 | 0% |

| 2,50,001 – 5,00,000 | 5% |

| 5,00,001 – 10,00,000 | 20% |

| Above 10,00,000 | 30% |

Key deductions available: Section 80C (₹1.5 lakh), Section 80D (health insurance), HRA, LTA, home loan interest (up to ₹2 lakh for self-occupied property).

New Tax Regime (default regime from 2023):

| Total Income (₹) | Tax Rate |

|---|---|

| 0 – 4,00,000 | 0% |

| 4,00,001 – 8,00,000 | 5% |

| 8,00,001 – 12,00,000 | 10% |

| 12,00,001 – 16,00,000 | 15% |

| 16,00,001 – 20,00,000 | 20% |

| 20,00,001 – 24,00,000 | 25% |

| Above 24,00,000 | 30% |

Rebate under Section 87A ensures zero tax liability for taxable income up to ₹12 lakh. Standard deduction of ₹75,000 is available for salaried individuals. Most other deductions (80C, 80D, HRA, LTA, home loan interest) are not allowed.

The Confusion of Choice

In theory, choice empowers taxpayers. In practice, it creates paralysis. As the Economic Times noted ahead of Budget 2026, “those paying home loan EMIs, insurance premiums, rent or investing in long-term small savings schemes, are still in confusion whether they should continue with the old tax regime or shift to the new.”

This confusion is rational. The optimal regime depends on specific expenses that vary from year to year. A taxpayer with a large home loan and high medical insurance premiums may benefit from the old regime. A young renter with few deductions will almost certainly pay less under the new regime. But predicting which expenses will materialize in a given financial year—and whether they will exceed the threshold that makes the old regime worthwhile—requires forecasting that many households cannot do.

The Budget 2026 Status Quo

Expectations ahead of Budget 2026 were substantial. Industry bodies like PHDCCI proposed radical restructuring: a 20 percent maximum rate for incomes up to ₹30 lakh, with 25 percent for ₹30-50 lakh and 30 percent above ₹50 lakh. Taxpayers hoped for an increase in the 30 percent slab threshold from ₹24 lakh to ₹35 lakh or even ₹50 lakh.

The Budget delivered none of these changes. Slabs remained unchanged under both regimes. The government’s message was clear: after significant relief in 2023 (increasing the rebate limit to ₹7 lakh) and 2025 (raising the zero-tax threshold to ₹12 lakh), the tax structure would be allowed to settle before further revisions.

For the middle class, this was disappointing but not disastrous. The 2025 changes had already made the new regime attractive for most salaried employees without major deductions. The 2026 Budget’s focus shifted from rate cuts to compliance simplification—a quieter but arguably more meaningful form of relief.

SECTION 3: COMPLIANCE RELIEF — THE BUDGET 2026 CHANGES THAT MATTER

TCS Reductions for Education and Medical Remittances

One of the most significant middle-class relief measures in Budget 2026 was the reduction in Tax Collected at Source (TCS) rates on overseas remittances. For families sending children abroad for education, the TCS rate was reduced from 5 percent to 2 percent.

This matters because TCS is not an additional tax—it is a collection mechanism, credited against final tax liability. However, the reduction eases cash flow constraints. A family remitting ₹20 lakh for tuition fees would previously have paid ₹1 lakh in TCS upfront, needing to claim credit when filing returns. Under the new rate, the upfront payment is ₹40,000—a meaningful difference for households managing liquidity.

Similarly, TCS on overseas tour packages was standardized at 2 percent, replacing the earlier structure of 5 percent on the first ₹10 lakh and 20 percent beyond that. This simplifies budgeting for international travel, though the impact on the middle class is smaller given that foreign holidays remain a luxury for most.

Extended Return Filing Deadlines

Under the new Income Tax Act, 2025 (effective April 1, 2026), the deadlines for filing returns have been rationalized and extended.

| Type of Assessee | Due Date |

|---|---|

| Companies and audit cases | November 30 |

| Non-audit business cases and trusts | August 31 |

| Salaried individuals (ITR 1 and 2) | July 31 |

More significantly, the deadline for filing revised returns has been extended from December 31 to March 31 of the assessment year. A taxpayer who discovers an error in their July-filed return now has until the following March to correct it—a substantial relaxation that reduces the anxiety of “getting it wrong.”

Belated returns (filed after the due date but before December 31 of the assessment year) attract a late fee of ₹1,000 for incomes up to ₹5 lakh and ₹5,000 for higher incomes.

Simplified Forms and Reduced Litigation

The rollout of the Income Tax Act, 2025, promised redesigned return forms that ordinary taxpayers could file “without professional assistance.” Whether this promise will be fulfilled remains to be seen, but the intent—to reduce dependence on tax consultants for straightforward filings—is clear.

Other compliance simplifications include:

-

Common orders for assessment and penalty from Assessment Year 2027-28, reducing multiple proceedings for underreporting of income.

-

Immunity from penalties for minor defaults, with maximum imprisonment for remaining offenses capped at two years.

-

Conversion of certain penalties to fees (e.g., non-furnishing of transfer pricing reports), decriminalizing technical violations.

SECTION 4: THE OLD REGIME SURVIVAL — ALLOWANCES GET A BOOST

The Draft Income-tax Rules, 2026

While the Budget left tax slabs unchanged, the Draft Income-tax Rules, 2026 (released February 7, 2026) proposed significant increases in various allowances—but only for taxpayers in the old regime.

| Benefit / Allowance | Old Limit | New (Proposed) Limit |

|---|---|---|

| Interest-free/concessional loan exemption | ₹20,000 | ₹2,00,000 |

| Meal per meal exemption | ₹50 | ₹200 |

| Gift voucher annual exemption | ₹5,000 | ₹15,000 |

| Children education allowance (per child/month) | ₹100 | ₹3,000 |

| Children hostel allowance (per child/month) | ₹300 | ₹9,000 |

| Transport allowance cap (70% of allowance) | ₹10,000/month | ₹25,000/month |

These changes, if approved, would substantially increase take-home pay for employees who structure their compensation to maximize allowances. A taxpayer with two children could claim ₹72,000 annually for education allowance (2 children × ₹3,000 × 12 months) and ₹2,16,000 for hostel allowance—compared to just ₹2,400 and ₹7,200 under the old limits.

The Geographic Expansion of HRA

The Draft Rules also propose expanding the list of cities eligible for the higher 50 percent House Rent Allowance (HRA) exemption. Currently, only Mumbai, Delhi, Kolkata, and Chennai qualify. The new rules would add Bengaluru, Hyderabad, Pune, and Ahmedabad—recognizing that housing costs in these IT and manufacturing hubs now rival the four metros.

For a Bengaluru-based taxpayer with a ₹15 lakh salary paying ₹3 lakh annual rent, the HRA exemption would increase from ₹2.4 lakh to ₹3 lakh under the proposed rules. Combined with the enhanced allowances, CA Avinash Kumar Rao’s calculations suggest an additional tax saving of ₹88,733 compared to the old rules, bringing total tax liability down to ₹41,496—significantly lower than the new regime’s ₹97,500.

The Strategic Implication

The Draft Rules reveal an unstated government strategy: preserving the old regime as a viable option for those who can navigate its complexity, while nudging others toward the simplicity of the new regime. The enhanced allowances make the old regime dramatically more attractive—but only for employees whose employers are willing to restructure compensation packages to maximize these benefits.

This creates a new form of inequality: between employees of large, sophisticated companies (which will adjust compensation structures) and those of smaller firms (which will not). The middle-class anxiety shifts from “which regime?” to “does my employer offer the allowances I need?”

SECTION 5: THE SAVINGS DILEMMA — SECTION 80C AND THE INFLATION PROBLEM

The Frozen Limit

Section 80C, the primary deduction for savings, has remained at ₹1.5 lakh since 2014. Adjusted for inflation, this limit is now worth less than half what it was when introduced. A taxpayer who maxes out 80C today is saving substantially less in real terms than a taxpayer who maxed it out a decade ago.

The list of eligible instruments is extensive: PPF, EPF, ELSS mutual funds, life insurance premiums, National Savings Certificate, Sukanya Samriddhi Yojana, tuition fees for children, and principal repayment on home loans. Yet the total deduction across all these cannot exceed ₹1.5 lakh—forcing taxpayers to choose which savings goals to prioritize.

The Home Loan Trap

The interaction between 80C and home loan principal repayment creates a particular form of middle-class anxiety. For many households, the EMI’s principal component alone exceeds the 80C limit. Once the home loan deduction is claimed, no room remains for other 80C savings—PPF contributions, ELSS investments, children’s tuition fees—all must be sacrificed.

Tax expert Abhishek Soni notes that “those paying home loan equated monthly instalments (EMIs), insurance premiums, rent or investing in long-term small savings schemes, are still in confusion” about which regime to choose. The old regime allows the home loan deduction but requires navigating the complexity. The new regime offers simplicity but denies the deduction entirely.

Expert Demands for Budget 2026

Ahead of the Budget, experts made several demands regarding savings deductions:

-

Increase Section 80C limit to ₹2.5 lakh or ₹3 lakh to account for inflation and encourage long-term savings.

-

Allow select deductions under the new regime such as health insurance (80D) and home loan interest, “to make it more attractive without compromising simplicity.”

-

Increase Section 80D limits for health insurance premiums, as medical inflation has far outpaced the current caps.

None of these demands were met in Budget 2026. The 80C limit remains frozen. The new regime continues to exclude almost all popular deductions. The message is clear: the government is prioritizing revenue collection and administrative simplicity over incentivizing household savings.

SECTION 6: HEALTHCARE AND HOUSING — THE UNMET DEMANDS

Section 80D and Rising Medical Costs

Healthcare inflation in India has consistently outstripped general inflation for years. Hospitalization costs, diagnostic tests, and medicines have become significantly more expensive. Yet the deduction for health insurance premiums under Section 80D remains capped at ₹25,000 for self, spouse, and dependent children, and ₹50,000 for parents (₹75,000 if parents are senior citizens).

The TaxGuru pre-budget wishlist highlighted a specific anomaly: senior citizens enjoy an enhanced TDS threshold on interest income (₹1 lakh under Section 194A) but the deduction limit under Section 80TTB (interest income deduction for seniors) remains at ₹50,000—unchanged despite being “not aligned with this policy approach.”

More broadly, the wishlist argued that “the deduction under Section 80D should be revised upwards to ₹1,00,000, considering the inflation in the economy,” and that the benefit should be extended to the new tax regime. Neither demand was met in Budget 2026.

Home Loan Interest: The 80C Interaction

The deduction for home loan interest (up to ₹2 lakh for self-occupied property) remains available only under the old regime. The principal repayment component, eligible under 80C, also counts toward the ₹1.5 lakh limit—creating the trade-off described above.

For a middle-class family with a ₹50 lakh home loan at 8.5 percent interest, the annual interest component in early years is approximately ₹4.2 lakh—far exceeding the ₹2 lakh deduction limit. The excess offers no tax benefit. This is a structural feature of the tax code, not an oversight, but it creates a sense of unfairness among homeowners who see wealthy individuals deducting far larger amounts on multiple properties.

SECTION 7: CAPITAL GAINS AND THE SMALL INVESTOR

The Equity Investment Landscape

The middle class has increasingly turned to equity markets for long-term wealth creation. Mutual funds, particularly ELSS (tax-saving) funds, have become popular. However, the taxation of capital gains creates complexity that deters some small investors.

Under current rules:

-

Short-term capital gains (holding period <12 months) on listed equity shares and equity-oriented funds are taxed at 20 percent (increased from 15 percent in recent years).

-

Long-term capital gains (holding period ≥12 months) are taxed at 12.5 percent, with an exemption for gains up to ₹1.25 lakh per year.

The STT Increase

Budget 2026 increased Securities Transaction Tax (STT) on futures and options trading—0.05 percent on futures (up from 0.02 percent) and 0.15 percent on options (up from 0.1 percent).

This primarily affects active traders rather than long-term investors. However, the increase signals the government’s discomfort with speculative trading and its willingness to tax financial transactions more heavily—a trend that could extend to other capital market activities in future budgets.

The Rebate Exclusion Problem

A significant grievance among small investors is that the Section 87A rebate (which zeroes out tax for incomes up to ₹12 lakh under the new regime) does not apply to capital gains taxed at special rates under Sections 111A and 112A.

As the TaxGuru wishlist noted, “taxpayers with total income comprising largely of equity-linked capital gains may not be able to fully avail the rebate benefit, even where their overall income remains within the effective ‘no-tax’ threshold.” This creates “an unintended disparity between different classes of taxpayers, particularly small and retail investors” who increasingly rely on capital market returns.

The wishlist proposed that “the rebate under Section 87A be extended to include tax payable on income chargeable under Sections 111A and 112A, at least up to the specified income threshold.” No such extension was announced in Budget 2026.

SECTION 8: SENIOR CITIZENS — THE FORGOTTEN TAXPAYERS

The TDS-Deduction Mismatch

Senior citizens (aged 60 and above) occupy a distinct position in the tax code, with higher exemption limits and special provisions. However, anomalies persist.

The TDS threshold on interest income under Section 194A was enhanced to ₹1 lakh for senior citizens via the Finance Act, 2025. This means banks will not deduct tax at source on interest income up to ₹1 lakh. However, the deduction limit under Section 80TTB—which allows senior citizens to deduct interest income up to a specified amount—remains at ₹50,000.

“This misalignment continues to impose tax and compliance burdens even on senior citizens whose total income is modest, with medical and living expenses rising sharply with age,” the TaxGuru analysis noted. The recommendation to raise the 80TTB limit to ₹1 lakh was not adopted.

The Gift Taxation Threshold

Section 56(2)(x) provides that gifts received from non-relatives exceeding ₹50,000 in a financial year are taxable as income from other sources. This threshold was last revised in Budget 2006.

“Thus, considering the inflation and increased cost of living, the threshold limit should be enhanced to ₹1,50,000,” the wishlist proposed. This is particularly relevant for senior citizens, who may receive gifts from children for medical expenses or daily living. The threshold remains unchanged.

Family Settlements and Capital Gains

The wishlist also noted that “Section 47 does not explicitly provide for an exemption for assets transferred pursuant to a family settlement amongst relatives,” despite courts having ruled in favor of assessees that such settlements do not attract capital gains. The recommendation to “explicitly include family settlements” to reduce litigation—relevant for senior citizens dividing assets among heirs—was not addressed.

SECTION 9: THE INTERNATIONAL DIMENSION — NRIS AND FOREIGN ASSETS

TCS Rationalization for Remittances

The reduction in TCS rates for overseas education and medical treatment remittances from 5 percent to 2 percent benefits not just students but the families supporting them—including NRIs sending money to India for family expenses and Indian residents sending money abroad.

The Liberalised Remittance Scheme (LRS) threshold for TCS remains at ₹10 lakh per financial year. Remittances up to ₹10 lakh for education and medical treatment attract 0 percent TCS; above that, the new 2 percent rate applies. For other purposes (excluding education/medical), the 20 percent TCS rate applies to amounts exceeding ₹10 lakh.

Foreign Asset Disclosure Scheme

Budget 2026 introduced a time-bound scheme for declaration of foreign assets and foreign-sourced income, offering “limited immunity from penalty and prosecution under the Black Money Act” for those who come forward.

The scheme provides relief for “small taxpayers, former students having dormant foreign bank accounts, ESOP and Restricted Stock Unit (RSU) holders of foreign companies.” Prosecution provisions are not applicable for non-disclosure when the aggregate value of assets (other than immovable property) does not exceed ₹20 lakh.

This is a significant relaxation, acknowledging that many middle-class professionals who worked abroad or received foreign stock compensation may have inadvertently violated disclosure requirements. The one-time scheme allows them to regularize their status without facing criminal prosecution.

SECTION 10: THE CENTRAL QUESTION — REVENUE OR RELIEF?

The taxation of savings and the middle class in India reflects a fundamental tension between two competing objectives: maximizing government revenue and incentivizing household savings.

The Revenue Imperative

India’s tax-to-GDP ratio remains low by international standards. The government faces immense pressure to fund welfare schemes, infrastructure, and defense without increasing debt. Direct taxes on individuals are a relatively small portion of total revenue, but they are a politically visible and administratively straightforward source.

Keeping the 80C limit frozen, refusing to raise slabs, and limiting deductions under the new regime all serve the revenue imperative. Every rupee of deduction claimed is a rupee not collected. For a government facing fiscal constraints, expanding deductions is politically difficult.

The Savings Imperative

India’s household savings rate has been declining in recent years. The shift from defined-benefit pensions (guaranteed by employers or the state) to defined-contribution schemes (NPS, EPF) places the burden of retirement planning squarely on individuals. Without adequate savings, the elderly face poverty and dependence.

The tax code’s original purpose—to encourage long-term savings—remains valid. The failure to adjust deduction limits for inflation undermines this purpose, discouraging the very behavior the government claims to want.

The Unanswered Question

The central question of this topic remains unresolved: Is India’s tax system designed to encourage savings or to maximize revenue?

The 2026 Budget suggests the government has prioritized revenue and simplicity over savings incentives. Slabs unchanged. 80C frozen. New regime deductions minimal. Compliance eased but structural incentives for savings weakened.

Yet the Draft Rules on allowances suggest a different path—one where compensation restructuring, not deduction claiming, becomes the primary mechanism for tax-efficient savings. This shift advantages employees of large, sophisticated companies over those in smaller firms. It advantages those with access to financial advice over those without.

The middle class, caught between these competing pressures, continues to save—not because the tax code encourages it, but because the alternative is financial insecurity in old age. The anxiety that characterizes middle-class tax discourse is not primarily about the amount of tax paid. It is about the complexity of a system that seems designed to be navigated only by professionals, the unpredictability of annual changes, and the fear that one wrong step will trigger a notice from the Income Tax Department.

A tax system that requires professional assistance to optimize is not a system that serves the middle class. The 2026 Budget’s compliance simplifications are a step in the right direction—but only a step. The deeper reforms—indexing deduction limits to inflation, simplifying the dual regime, expanding the new regime’s deductions for healthcare and housing—remain for future budgets.

SUMMARY TABLE: KEY TAX PROVISIONS AFFECTING MIDDLE-CLASS SAVINGS

| Provision | Current Status | Budget 2026 Change | Impact on Middle Class |

|---|---|---|---|

| New regime slabs (0-4-8-12-16-20-24 lakh) | No change | None | Status quo; zero tax up to ₹12 lakh via rebate |

| Old regime slabs (2.5-5-10-10+ lakh) | No change | None | Status quo; Section 80C available |

| Section 80C limit | ₹1.5 lakh | No change | Frozen since 2014; real value eroded by inflation |

| Section 80D limit | ₹25k (self), ₹50k (parents) | No change | Healthcare inflation outpaces deduction limits |

| TCS on education/medical remittances | 5% | Reduced to 2% | Eases cash flow for families with overseas students |

| Revised return deadline | Dec 31 of assessment year | Extended to March 31 | More time to correct errors, reduces anxiety |

| STT on futures/options | 0.02%/0.1% | Increased to 0.05%/0.15% | Discourages speculative trading |

| Standard deduction (new regime) | ₹75,000 (salaried) | No change | Available only under new regime |

| HRA exemption cities | 4 metros | Proposed: +4 cities | Benefits employees in Bengaluru, Hyderabad, Pune, Ahmedabad |

| Children education allowance | ₹100/month | Proposed: ₹3,000/month | Major benefit for parents under old regime |

| Children hostel allowance | ₹300/month | Proposed: ₹9,000/month | Major benefit for parents under old regime |