GST COMPLIANCE BURDEN ON SMALL BUSINESSES

GST COMPLIANCE BURDEN ON SMALL BUSINESSES Operational and Financial Challenges Faced by MSMEs On January 1, 2026, India’s Goods and Services Tax framework underwent its most significant transformation since its

GST COMPLIANCE BURDEN ON SMALL BUSINESSES

Operational and Financial Challenges Faced by MSMEs

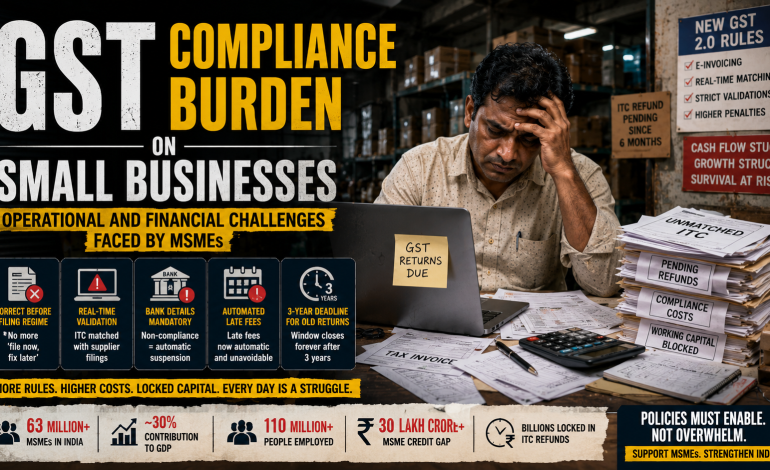

On January 1, 2026, India’s Goods and Services Tax framework underwent its most significant transformation since its 2017 launch. The system moved decisively from a “file now, fix later” approach to a “correct before filing” regime . Returns could no longer be filed with minor mismatches and corrected later. Input Tax Credit claims would be validated in real-time against supplier filings. Bank account details became mandatory, with non-compliance triggering automatic registration suspension. Late fees became automated and unavoidable. And a three-year hard deadline was imposed on filing old returns, after which the window would close forever .

For large corporations with dedicated tax departments and integrated ERP systems, these changes represented an efficiency gain—automated validations replacing manual reconciliations. For India’s 63 million micro, small, and medium enterprises—the backbone of the economy, contributing nearly 30 percent to GDP and employing over 110 million people—they represented something else entirely: a compliance cliff .

The numbers told a story of deepening distress. The MSME sector faced a staggering ₹30 lakh crore credit gap, further aggravated by billions of rupees locked in unrefunded input tax credits due to the GST’s inverted duty structure . Food processing companies paid 18 percent GST on packaging, logistics, and cold storage while selling finished products taxed at just 5 percent. Small e-commerce sellers paid 18 percent on platform fees and logistics while selling garments and handicrafts at 5 percent . Manufacturers waited months for refunds of the tax differential, despite the prescribed 30-day timeline . In industrial clusters across Punjab, Maharashtra, and Gujarat, small manufacturing units were being forced to periodically halt operations because working capital remained tied up in pending ITC claims .

Industry bodies, in their pre-Budget submissions, painted a picture of structural fragility. The Federation of Indian Micro and Small & Medium Enterprises warned that “without these interventions, demand growth risks bypassing the MSME sector” . The India SME Forum argued that “compliance costs under GST remain disproportionately high for smaller firms, locking up working capital and discouraging formalisation despite wider Udyam registration” . A partner at Shardul Amarchand Mangaldas, writing in the Hindustan Times, observed that for a rural MSME, the progression of GST 2.0—with its e-invoicing, real-time data matching, and system-driven validations—had created “formidable barriers to compliance” .

This article examines the operational and financial challenges that GST compliance imposes on small businesses in India. It explores the compliance cost structure, the liquidity crisis driven by the inverted duty structure, the transition to a system-driven regime, and the fundamental question of whether India’s tax architecture is designed for the convenience of large corporations or the survival of its.

WHAT – GST compliance burden refers to the operational, financial, and administrative costs that businesses incur to meet the requirements of India’s indirect tax system. For small businesses, this burden is disproportionately high relative to their size, including monthly return filings (GSTR-1, GSTR-3B), annual returns (GSTR-9, GSTR-9C), e-invoicing, real-time reconciliation with supplier filings, input tax credit matching, and maintaining audit trails. The burden encompasses both direct costs (professional fees, software subscriptions) and indirect costs (working capital locked in unrefunded credits, management time diverted from production).

WHO – Micro, small, and medium enterprises (MSMEs)—defined by investment in plant and machinery or annual turnover—form the core constituency affected by GST compliance burdens. Industry bodies (FISME, India SME Forum, Empower India, PHDCCI) advocate for their interests. The GST Council, comprising central and state finance ministers, sets policy. The Central Board of Indirect Taxes and Customs (CBIC) administers the system. Tax professionals (CAs, GST practitioners) and GST Suvidha Providers (GSPs) offer compliance services. Export-oriented MSMEs face additional compliance layers through RoDTEP and refund mechanisms.

WHEN – The GST regime was introduced on July 1, 2017. Major rationalization occurred in September 2025. The shift to a system-driven compliance regime with automated validations, return blocking, and strict timelines took effect on January 1, 2026 . The Union Budget 2026-27 was presented on February 1, 2026, with MSMEs pressing for simplification measures. Current data on the ₹30 lakh crore credit gap and blocked ITC refunds reflects the situation as of mid-2026 .

WHERE – Across India, with particular intensity in manufacturing clusters in Punjab, Maharashtra, Gujarat, Tamil Nadu, Karnataka, and Uttar Pradesh. E-commerce-related compliance burdens affect small online sellers nationwide, with platforms like Amazon, Flipkart, and Meesho central to the digital commerce ecosystem . Export-oriented MSMEs face additional challenges related to GST refunds at ports and customs checkpoints.

WHY – The GST compliance burden on small businesses arises from several structural features: the inverted duty structure (inputs taxed higher than outputs, leading to locked-in credits), the shift from trust-based to technology-driven enforcement, the high cost of professional compliance support relative to MSME margins, delayed GST refunds that tie up working capital, fragmented enforcement across states, and the disproportionate impact of penalties and interest on small businesses with thin cash buffers.

HOW – Through monthly filing requirements on the GST portal; e-invoicing mandates for businesses above turnover thresholds (currently ₹10 crore); reconciliation of GSTR-1 (sales) with GSTR-3B (summary return) and GSTR-2B (purchase credits); automated validation checks that block returns if mismatches exceed thresholds; late fee auto-calculation; registration suspension for non-compliance with bank detail requirements; and annual return filing with audit requirements for businesses above prescribed turnover.

SECTION 1: THE COMPLIANCE COST STRUCTURE — WHAT SMALL BUSINESSES ACTUALLY PAY

The cost of GST compliance for a small business extends far beyond the tax liability itself. It encompasses professional fees, software subscriptions, internal staff time, and the opportunity cost of management attention diverted from operations.

The Direct Cost Breakdown

A comprehensive GST compliance guide for 2026 breaks down the monthly costs that small businesses face :

| Method | Monthly Cost (₹) | Best For |

|---|---|---|

| DIY on GST Portal | ≈ 2,000 | Sole founders, <100 invoices |

| Cloud Accounting Software | 499 – 1,999 | Tech-savvy teams |

| Part-Time Accountant | 6,000 – 10,000 | Growing startups |

| CA Retainer | 15,000 – 30,000 | Funded SMEs |

For a micro-enterprise at the lower end of the spectrum, ₹2,000 per month translates to ₹24,000 annually—a significant sum when profit margins are thin. For a small business that requires professional support, the cost rises to ₹72,000-₹1.2 lakh annually for a part-time accountant, or ₹1.8-₹3.6 lakh for a CA retainer.

These figures exclude one-time costs: GST registration (₹1,000-₹5,000 for professional fees, plus ₹1,000-₹2,000 for Digital Signature Certificate), software implementation costs, and training expenses .

The Hidden Cost: Management Time

Beyond direct financial costs, compliance consumes management bandwidth. As the India SME Forum noted in its pre-Budget submission, “frequent filings, complex audits and delays in reacting GST registrations have made compliance more of a hurdle than an enabler” . The owner of a small manufacturing unit cannot spend hours reconciling invoices with supplier filings while also managing production, quality control, and customer acquisition.

A partner at Shardul Amarchand Mangaldas & Co., writing in the Hindustan Times, observed that unlike larger firms with dedicated tax departments, “MSMEs rarely possess in-house expertise, and the expense of engaging external consultants or procuring compliance software further inflates their overhead costs” .

The Penalty Exposure

The financial risk of non-compliance is substantial. Penalties start at ₹10,000 or the evaded tax—whichever is higher. Late filing of GSTR-3B attracts ₹50-₹200 per day, capped at 0.25 percent of turnover. Incorrect invoice data can cost up to ₹25,000 per error. Wrongful ITC claims require repayment plus 24 percent interest .

For a small business with thin margins, a single compliance error can wipe out months of profit. The India SME Forum’s president, Vinod Kumar, captured the frustration: “Micro and small enterprises face GST compliance costs that are often out of proportion to their size, straining working capital and weakening incentives to formalise them” .

SECTION 2: THE LIQUIDITY CRISIS — WHEN INPUT TAX CREDIT BECOMES A TRAP

The most severe financial challenge facing MSMEs under GST is not the tax rate but the timing of cash flows. Under the accrual-based framework, tax obligations crystallize at the moment an invoice is raised—not when payment is actually received.

The Accrual Problem

As the Hindustan Times analysis explains, “Under the prevailing accrual-based framework, tax obligations crystallise at the moment an invoice is raised, rather than when payment is actually received. For MSMEs routinely subjected to delayed payments from larger corporate buyers—delays that can extend from 90 to 120 days—this creates a substantial cash flow shortfall. Small business owners are often compelled to take on expensive working capital borrowings simply to meet their GST payment deadlines, thereby depleting the financial reserves necessary for sustained operations” .

The problem is compounded by the 45-day payment rule under the MSMED Act. While the rule exists to protect small suppliers, its enforcement remains weak. The India SME Forum has urged the government to tighten enforcement, citing “persistent delays by large buyers that trap MSME capital in receivables” .

The Inverted Duty Structure

Even when payments are timely, the inverted duty structure creates a permanent liquidity drag. Empower India, a public policy think tank, explained the mechanism: “The IDS refers to a tax structure where GST paid on raw materials and services is higher than the tax levied on finished goods. Manufacturers purchasing inputs at 18 percent GST while selling finished products taxed at 5 percent are forced to wait months for refunds, despite the prescribed 30-day timeline” .

The sectors most affected include food processing (finished products at 5 percent, packaging and logistics at 18 percent), e-commerce (small sellers paying 18 percent on platform fees while selling products at 5 percent), renewable energy (solar equipment at 5 percent, steel and engineering services at 18 percent), and pharmaceuticals (where post-GST 2.0 tax inversions are impacting manufacturing capacity) .

The Refund Mechanism Failure

The problem is not merely structural—it is also administrative. The refund mechanism under Section 54(3) of the CGST Act permits ITC refunds only for input goods, explicitly excluding input services and capital goods . This creates a “permanent cost disadvantage” for small businesses that cannot offset the tax differential through operational efficiencies.

Empower India’s Director General, K Giri, painted a grim picture: “India’s small businesses are the backbone of our economy—and they are being slowly asphyxiated by a tax structure that punishes production” . The organization warned that prolonged GST inversion could trigger “factory shutdowns, loss of livelihoods and further stress on India’s small business ecosystem” .

The ₹30 Lakh Crore Credit Gap

The scale of the crisis is staggering. Empower India estimated that the MSME sector faces a ₹30 lakh crore credit gap, “further aggravated by blocked ITC refunds” . For context, this is roughly equivalent to the annual GDP of a mid-sized economy. In industrial clusters across Punjab, Maharashtra, and Gujarat, small manufacturing units are “already being forced to periodically halt operations because working capital remains tied up in pending ITC claims” .

SECTION 3: THE SYSTEM-DRIVEN REGIME — JANUARY 2026 CHANGES

The compliance landscape shifted dramatically on January 1, 2026, when the GST system moved from a trust-based to a technology-enforced framework .

The “Correct Before Filing” Mandate

Under the previous regime, businesses could file returns with minor mismatches and correct them later. The new system eliminates this flexibility entirely. As a GST compliance advisory explained, “The portal will not allow mistakes anymore. Returns can get blocked instantly. No flexibility for corrections after filing” .

The most significant change affects Input Tax Credit claims. The portal now validates ITC claims in real-time, checking whether the credit is available in the ledger, whether the supplier has filed returns, and whether balances match. “If mismatch → GSTR-3B will not be filed. ITC is now validated, not assumed” .

Return Blocking and Hard Stops

The system now blocks return filing under several conditions:

| Condition | Consequence |

|---|---|

| ITC claimed exceeds ledger balance | GSTR-3B filing blocked |

| RCM liability not paid | Return submission prevented |

| Negative balance in ledger | Filing window does not open |

| Bank details missing/unverified | Registration may be suspended |

A manufacturing firm that claims ITC based on purchase invoices but has not reconciled them with supplier filings will now find the portal blocking submission until the ledger data matches the claim .

The Three-Year Deadline

One of the most consequential changes is the three-year hard deadline on filing old returns. If a return remains unfiled for more than three years, the system will block it permanently. “No option to reopen the return. No penalty route to restore it. No manual intervention to bypass the restriction” .

For MSMEs that have carried old pending returns with the assumption that they could resolve them later, this rule eliminates that possibility. A company that failed to file returns for a period in FY 2022-23 and planned to rectify it in 2026 will find the system permanently blocking those filings .

Automatic Late Fees and Interest

Late fees are now automatically calculated by the portal, and returns cannot be submitted unless the fee is paid. Even NIL returns attract penalties if delayed . Interest is also auto-calculated and auto-populated in GSTR-3B, with no provision for manual reduction .

A small service provider who misses the monthly deadline by two weeks will now find the portal preventing return filing until the late fee is paid—making timely filing financially and operationally essential .

SECTION 4: THE E-INVOICING MANDATE — TECHNOLOGY AS BARRIER

For large corporations with integrated ERP systems, e-invoicing represents efficiency. For small businesses, it represents a formidable technological barrier.

The Threshold and Requirements

Businesses with turnover greater than ₹10 crore are required to generate e-invoices with a unique Invoice Reference Number (IRN) before dispatch . The threshold has progressively decreased from ₹500 crore to ₹100 crore to ₹50 crore to ₹20 crore to ₹10 crore—bringing more MSMEs into the net with each reduction.

If there is a mismatch between the e-invoice and GSTR-1 for that month, the system generates an auto-notice. Unlike the previous regime where notices required human initiation, these are automated and require formal responses.

The Compliance Layer

E-invoicing compliance does not end with IRN generation. Post-implementation gaps often include:

-

Invoice series not being reset annually

-

IRN data not reconciling with GSTR-1

-

Delays in reporting within prescribed timelines

-

Technical failures in API integration

For a small business without dedicated IT support, each of these represents a potential failure point. As the IRIS GST analysis noted, “With the ₹5 crore threshold bringing more businesses under e-invoicing from August 2023, many are exposed to risks not visible at the implementation stage” .

SECTION 5: THE E-COMMERCE DIMENSION — SMALL ONLINE SELLERS

Small online sellers face a distinct set of GST compliance challenges that their offline counterparts do not encounter.

The Platform Fee Burden

The India SME Forum flagged a critical issue: small businesses pay GST across multiple layers of their e-commerce operations, including warehousing, logistics, packaging, payment gateway charges, advertising, returns management, and platform commissions .

Unlike large technology platforms or integrated logistics operators, smaller enterprises “often lack access to complex tax structuring mechanisms, extensive legal teams or prolonged litigation capabilities” . The result is a structural disadvantage: large platforms can optimize their tax positions, while small sellers bear the full compliance burden.

The Competitive Neutrality Principle

The Forum argued that “GST policy must uphold the principle of competitive neutrality, where no participant in the value chain derives an unfair advantage through interpretational arbitrage or regulatory asymmetry” .

A recent ruling by the West Bengal Appellate Authority for Advance Ruling reinforced the need for such neutrality, holding that operationally similar logistics or courier activities should attract tax treatment aligned with their actual economic function rather than contractual classification alone .

The Practical Impact

Over 1.4 million small sellers operating on e-commerce platforms face the inverted duty burden, paying 18 percent GST on platform fees, packaging, and logistics while selling products such as garments, handicrafts, and food items taxed at 5 percent .

The India SME Forum warned that “any taxation structure that lowers indirect tax burdens for dominant digital intermediaries while ecosystem-related costs remain fully taxable for MSMEs raises concerns around market fairness” .

SECTION 6: THE HIDDEN RISKS — WHAT BUSINESSES DON’T SEE COMING

Beyond the visible compliance costs and liquidity pressures, several hidden risks have emerged in the 2026 GST environment.

The Timing Gap: When Businesses Actually Start Compliance

A common gap identified by compliance experts is the timing of when businesses begin their GST work each month. Typically, ITC and GST compliance activities begin only after the generation of GSTR-2B around the 14th of the following month, by which time suppliers have already filed their GSTR-1 on the 11th .

This delayed reconciliation means that any errors made by suppliers are identified late, leading to data gaps and mismatches. As a result, businesses often face blocked working capital and reduced ITC claims. The recommended approach is “proactive reconciliation using IMS data, allowing businesses to identify and address discrepancies even before vendors file their returns” .

The Over-Reliance on External Advisors

Another common risk is the assumption that engaging a Chartered Accountant fully insulates the business from compliance liability. While CAs play a critical role, there is often a misunderstanding about what their responsibility actually includes.

The IRIS GST analysis explains that a CA’s role is typically limited to “ensuring that returns are filed correctly based on the data provided.” However, several important activities fall outside this scope: monitoring whether vendors are filing their returns on time, tracking mismatches between invoices and portal data, internal data processing, and vendor communication .

“Because of this, a gap can develop between what the business assumes is being handled and what is actually being monitored. By the time an issue becomes visible during review or audit, it has usually been present in the system for months.” The analysis concludes: “Ultimately, while filing can be supported externally, ownership of compliance always remains with the business” .

The ERP Assumption

Many small businesses assume that implementing an ERP system ensures GST compliance. This is a dangerous assumption. ERP systems are designed for transaction processing, not compliance validation. They generate invoices and calculate tax but do not perform cross-party reconciliation, monitor IMS actions, or validate rate classifications dynamically .

“With GST 2.0 rate changes introduced in 2025, outdated ERP configurations can result in incorrect reporting over extended periods, often without immediate visibility. A dedicated compliance layer is no longer optional” .

The Notice Gap: When Problems Surface

GST notices in 2026 are rarely about recent filings. They are typically based on historical data (often 2-3 years old), pattern recognition across multiple periods, and accumulated inconsistencies. “By the time a notice is issued, the system has already analyzed and built a case” .

This means that a business that has been filing “on time” but inaccurately may have no indication of problems until a notice arrives for a period the management has long stopped monitoring. Early detection and continuous monitoring—rather than reactive corrections—have become essential.

SECTION 7: THE REFORM AGENDA — WHAT MSMES ARE DEMANDING

Ahead of the Union Budget 2026-27, industry bodies articulated a clear set of demands to address the GST compliance burden .

GST Rationalization

The Federation of Indian Micro and Small & Medium Enterprises pressed for “faster and automatic GST refunds, and relief on the upfront tax cost of plant and machinery” to unlock fresh investment across manufacturing clusters .

The India SME Forum proposed a “simplified GST regime for micro enterprises, including fewer filings, self-certification in place of audits and a lower effective tax incidence for the smallest units” . The association maintained that easier compliance would expand the formal base and improve working capital efficiency without materially impacting revenues.

Inverted Duty Correction

Empower India called for several structural reforms: broadening the refund scope under Section 54(3) to include input services and capital goods; redefining “Net ITC” to capture all input costs; rationalizing GST rates in sectors facing severe inversion; and introducing automated refund systems to improve working capital access for MSMEs .

The organization also called for the creation of a “dedicated IDS monitoring mechanism to identify emerging tax inversions before they evolve into larger systemic problems” .

Payment Protection

The India SME Forum urged the government to “tighten enforcement of the 45-day payment rule under the MSMED Act,” citing “persistent delays by large buyers that trap MSME capital in receivables.” Mandatory disclosure of payment timelines and statutory interest enforcement, it said, could unlock significant liquidity without fiscal cost .

Harmonized Interpretation Across States

The India SME Forum also called for “greater consistency in GST interpretation across states, arguing that fragmented enforcement practices increase uncertainty for companies operating across India’s digital marketplaces” . The organization sought “clearer interpretational guidance to ensure future compliance certainty” and “harmonised interpretation of tax rules across states” .

SECTION 8: THE EXPERT VIEW — GST 2.0 AS MATURATION OR BURDEN?

Tax experts are divided on whether the GST 2.0 changes represent necessary maturation or excessive burden.

The Maturation Argument

Abhishek A Rastogi, Founder of Rastogi Chambers, argued that “a second wave of GST and Customs restructuring may be necessary, focusing on pruning remaining inverted duty structures, merging overlapping slabs and simplifying compliance for MSMEs. The GST reform journey has reached a stage where fine-tuning, not fire-fighting, is required” .

Rajat Mohan, Senior Partner at AMRG & Associates, added that “revenue performance in 2026 is expected to be supported more by improved compliance, deeper formalisation and technology-led enforcement than by higher tax rates, with analytics-based matching across returns, e-invoicing and customs data playing a larger role in administration” .

The Burden Argument

However, Rajat Bose, Partner at Shardul Amarchand Mangaldas & Co., offered a more critical perspective in the Hindustan Times: “For large, technologically equipped corporations, these developments represent efficiency gains. For a rural MSME, however, they constitute formidable barriers to compliance. The increasingly exacting expectation of near-perfect compliance means that even a trivial clerical error on the part of a supplier can result in the blocking of Input Tax Credit for the purchasing MSME, thereby generating a trust deficit across the supply chain” .

Bose concluded that “GST 2.0 represents the maturation of India’s indirect tax architecture. Its ultimate success, however, will not be judged solely by revenue collection figures, but rather by the health and resilience of the MSME ecosystem it governs” .

SECTION 9: THE WAY FORWARD — BUILDING A FACILITATION MODEL

The way forward requires a shift from an enforcement-centric to a facilitation-centric regulatory model.

Policy Adjustments

Bose’s analysis offered specific recommendations: expanding the scope of the Composition Scheme or introducing a quarterly payment arrangement for a wider segment of MSMEs to meaningfully alleviate liquidity pressures; implementing a threshold-linked safe harbour provision for minor compliance discrepancies to prevent disproportionate penalisation of small businesses for immaterial errors; and bolstering the MSME Samadhaan portal to compel large buyers to settle GST-inclusive invoices within 45 days .

Technology as Enabler, Not Barrier

For technology to serve MSMEs rather than exclude them, platforms like Vayana GSP enable businesses to connect their internal systems with GST infrastructure through secure APIs . While technology cannot replace sound compliance practices, it can help reduce manual errors and streamline complex processes.

The Facilitation-First Model

Bose concluded: “Achieving a genuine balance between tax rationalisation and business sustainability demands a transition towards a facilitation-first regulatory model. By confronting the structural challenges of liquidity stress, inverted duty distortions, and disproportionate compliance costs, India can safeguard the role of its small businesses as the engine of inclusive economic growth” .

SECTION 10: THE CENTRAL QUESTION — REVENUE OR RESILIENCE?

The politics of GST compliance for small businesses reflects a fundamental tension between two competing priorities: maximizing revenue collection and preserving the resilience of the MSME sector.

The Revenue Imperative

The shift to system-driven compliance—with automated validations, return blocking, and strict timelines—has undoubtedly improved revenue collection. Inverted duty structures, while burdensome for small businesses, generate significant tax revenue that would be lost if rates were fully rationalized. The government’s fiscal constraints make revenue maximization a legitimate concern.

The Resilience Imperative

However, as Empower India’s analysis shows, the current structure is “slowly asphyxiating” the MSME sector. The ₹30 lakh crore credit gap, the factory shutdowns in Punjab, Maharashtra, and Gujarat, the 1.4 million small e-commerce sellers paying punitive effective rates—these are not efficiency gains. They are structural failures that, if unaddressed, will undermine the very productive capacity that generates tax revenue in the long term.

The Unanswered Question

The central question of this topic remains unresolved: Is India’s GST architecture designed for the convenience of large corporations or the survival of small businesses?

The answer will determine not just the compliance burden of 63 million MSMEs, but the health of an economy that depends on them for 30 percent of GDP and 110 million jobs. As the India SME Forum’s president argued, “The sustainable growth of India’s digital economy will depend on fairness, transparency and equal opportunity for enterprises of all sizes” . The same principle applies to the entire GST ecosystem.

GST 2.0 represents a choice. It can be a system that uses technology to exclude—raising barriers ever higher, automating small businesses out of formal markets. Or it can be a system that uses technology to include—simplifying compliance, automating refunds, and creating a level playing field. The choice is not technical. It is political. And it will determine whether India’s MSMEs survive as the engine of inclusive growth or are slowly crushed between the gears of an unforgiving tax machine.

SUMMARY TABLE: KEY GST COMPLIANCE CHALLENGES FOR MSMEs

| Challenge | Description | Impact | Source |

|---|---|---|---|

| Direct compliance cost | ₹2,000-₹30,000/month depending on method | Eats into thin MSME profit margins | IndiaFilings 2026 |

| Inverted duty structure | Inputs taxed at 18%, outputs at 5% | Blocks ITC, ties up working capital for months | Empower India 2026 |

| Delayed GST refunds | Refunds take months despite 30-day timeline | Forces periodic factory shutdowns | Empower India 2026 |

| ₹30 lakh crore credit gap | MSME sector credit gap aggravated by blocked ITC | Constrains growth and survival | Empower India 2026 |

| System-driven return blocking | Mismatches block GSTR-3B filing entirely | Prevents “file now, fix later” approach | IndiaFilings/Vayana 2026 |

| Three-year hard deadline | Returns >3 years old permanently blocked | Cannot correct old errors or claim historical ITC | IndiaFilings 2026 |

| Bank detail requirement | Missing/unverified bank details trigger registration suspension | Blocks e-way bills, e-invoicing, returns | Vayana 2026 |

| E-commerce platform burden | 18% GST on platform fees, logistics vs 5% on products | Disadvantage for small online sellers | India SME Forum 2026 |

| Professional dependency | CA retainer ₹15,000-30,000/month | Out of reach for micro-enterprises | IndiaFilings 2026 |

| ERP compliance gap | ERP systems don’t validate compliance | Hidden risk of incorrect reporting | IRIS GST 2026 |