STOCK MARKET GROWTH AND UNEQUAL PARTICIPATION

STOCK MARKET GROWTH AND UNEQUAL PARTICIPATION Who Benefits Most from Financial Market Expansion? In May 2026, the Securities and Exchange Board of India released a research paper that fundamentally changed

STOCK MARKET GROWTH AND UNEQUAL PARTICIPATION

Who Benefits Most from Financial Market Expansion?

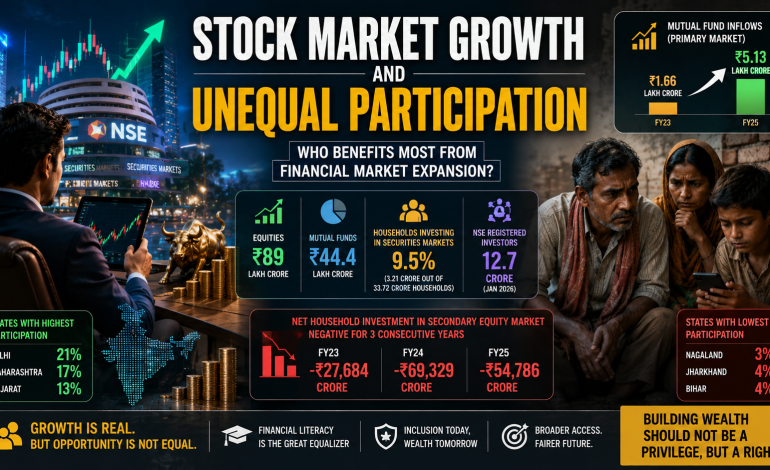

In May 2026, the Securities and Exchange Board of India released a research paper that fundamentally changed how we understand the scale of India’s retail investing boom. For years, official savings data had relied on simplified assumptions—attributing 35 percent of public equity issuances to households, 40 percent of corporate bond issuances, and largely ignoring secondary market transactions, SIP-driven mutual fund investments, ETFs, REITs, and InvITs altogether . The revised methodology, using actual transaction data from depositories, stock exchanges, and mutual fund registrars, revealed a staggering truth: household assets in securities markets stood at ₹141.34 lakh crore by FY25—with equities accounting for ₹89 lakh crore and mutual funds another ₹44.4 lakh crore .

The numbers paint a picture of spectacular growth. Mutual fund inflows through the primary market jumped from ₹1.66 lakh crore in FY23 to ₹5.13 lakh crore in FY25 . The National Stock Exchange’s registered investor base has nearly quadrupled over six years, reaching 12.7 crore by January 2026 . The post-pandemic investing wave is unmistakable.

Yet beneath these headline figures lies a more complicated story. The same SEBI survey that documented this growth also revealed that only 9.5 percent of Indian households invest in securities markets—just 3.21 crore out of 33.72 crore households . While 63 percent of households are aware of securities market products, the gap between knowledge and action remains vast. Participation is heavily concentrated in economically advanced states—Delhi at 21 percent, Maharashtra at 17 percent—while states like Nagaland languish at 3 percent .

The SEBI research paper also uncovered a counterintuitive finding: despite the surge in equity market participation, net household investments in the secondary equity market have remained negative for three consecutive years—-₹27,684 crore in FY23, -₹69,329 crore in FY24, and -₹54,786 crore in FY25 . Households are actively booking profits or reallocating capital even as participation surges.

This article examines the unequal distribution of stock market participation in India—who invests, who benefits, and who remains excluded. It explores the structural barriers that sustain this inequality, the shift from physical to financial assets, the emerging digital investor archetypes, and the fundamental question of whether India’s financial market expansion is building broad-based wealth or concentrating gains among the already affluent.

WHAT – Stock market participation inequality refers to the uneven distribution of equity and mutual fund investments across Indian households. While total market capitalization and retail investor numbers have grown dramatically, the share of households invested remains low at 9.5 percent . Participation varies significantly by geography, income, education, gender, and occupation. The question of who benefits from market expansion is not merely about returns—it is about which segments of society have access to the wealth-generating potential of financial markets.

WHO – The Securities and Exchange Board of India (SEBI) regulates markets and produces crucial data on investor participation. Registered investors on the NSE have reached 12.7 crore , but this counts individuals with demat accounts, not necessarily active investors. Salaried millennials form the single largest block of systematic investors through SIPs . Women have reached one-fourth of market participants, though their share of equity and mutual fund investors remains lower at 25 percent versus 65 percent for men . Gen Z and Tier-2+ city investors are growing fastest . The Economic Survey and RBI provide macro-level analysis of household savings patterns. Industry bodies and finfluencers influence retail investment behavior, with nearly 62 percent of prospective investors influenced by unregulated finfluencers .

WHEN – The post-pandemic investing wave (2020-2026) has seen unprecedented retail participation. Key data points: mutual fund inflows tripled from FY23 to FY25 ; NSE investor base nearly quadrupled in six years ; household financial savings share rose from 27 percent in FY23 to 33 percent in FY25 . The SEBI investor survey was released in January 2026, with the research paper on household savings following in May 2026 .

WHERE – Across India, with stark regional disparities. Maharashtra leads with 2 crore registered investors and 28.9 percent female participation . Delhi has the highest penetration at 21 percent of households . Goa, Mizoram, Chandigarh, and Sikkim show the highest female participation rates, exceeding 30 percent . Uttar Pradesh, despite ranking second in overall investors, has female participation below the national average at 19 percent . North India leads with 4.6 crore registered investors, followed by West (3.7 crore), South (2.7 crore), and East (1.5 crore) .

WHY – Multiple structural factors drive unequal participation: income and wealth thresholds that exclude bottom-half households; educational disparities (postgraduate penetration at 27 percent versus lower education levels at much lower rates) ; geographic concentration of financial infrastructure; gender gaps in income, confidence, and product design ; occupational differences (salaried individuals at 23 percent penetration versus self-employed at lower rates) ; and behavioral factors including risk aversion and lack of trusted advisory services .

HOW – Through multiple channels: Systematic Investment Plans (SIPs) have become the dominant mode for salaried millennials ; direct equity investing via discount brokers; mutual funds through distributors and online platforms; Employer-linked retirement savings (EPF, NPS); and new instruments like REITs, InvITs, and bonds . Digital platforms now account for ~80 percent of direct equity investors and ~35 percent of mutual fund investors .

SECTION 1: THE PARTICIPATION GAP — 9.5% OF HOUSEHOLDS, 90% OF GAINS?

The most fundamental fact about India’s stock market expansion is also the most sobering: only 9.5 percent of Indian households invest in securities markets . Out of 33.72 crore households, just 3.21 crore have any exposure to equities, mutual funds, or corporate bonds .

The Awareness-Participation Disconnect

The SEBI investor survey reveals a striking paradox: while 63 percent of Indian households are aware of securities market products, actual investment remains stuck at single-digit levels . Mutual funds and ETFs have 53 percent awareness but only 6.7 percent penetration. Listed equities have 49 percent awareness but just 5.3 percent household penetration .

This gap between awareness and action suggests that the barriers are not merely informational. Even when households know about investment products, they do not—or cannot—invest. The reasons include income constraints, lack of trust, perceived complexity, and the absence of accessible, trustworthy advisory services.

The Geographical Divide

Participation is heavily concentrated in economically advanced, urbanized states :

| State/Region | Household Participation Rate |

|---|---|

| Delhi | 21% |

| Maharashtra | 17% |

| Goa | 16% |

| Gujarat | 15% |

| Nagaland | 3% |

| Uttarakhand | 4.5% |

| Meghalaya | 4.5% |

The urban-rural gap is equally stark. Urban households report 74 percent awareness of at least one securities product, compared with 56 percent in rural areas. Penetration is highest in the top nine metros at 23 percent, followed by 10–40 lakh towns at 16 percent, and 5–10 lakh towns at 14 percent .

The Education Gradient

Education is perhaps the strongest predictor of market participation. Among graduates, penetration stands at 19 percent; among postgraduates, it jumps to 27 percent . For those with lower education levels, participation drops dramatically. This creates a self-reinforcing cycle: those with higher education earn more, save more, invest more, and benefit more from market growth—widening the wealth gap further.

The Occupational Divide

Salaried individuals lead with 23 percent penetration—more than double the national average . The self-employed and business owners show lower participation, despite having potentially higher incomes. This suggests that predictable, documented income—not just income level—is a prerequisite for market participation. The formal salaried class has access to employer-linked financial products, easier KYC processes, and more stable cash flows that enable systematic investing through SIPs.

What the 90% Miss

For the 30.51 crore households outside the securities market, the opportunity cost is substantial. Over the past decade, the BSE equity market capitalization surged from around ₹101 lakh crore in FY2014–15 to nearly ₹4,701 lakh crore by October 2025 . Mutual fund AUM expanded from ₹12 lakh crore in 2015 to ₹79 lakh crore in September 2025 .

These gains have been captured predominantly by the already-invested minority. The bottom half of Indian households—those without access to markets—have watched from the sidelines as asset prices soared, their savings stuck in low-yield bank deposits or physical assets with lower returns.

SECTION 2: THE SHIFT FROM PHYSICAL TO FINANCIAL ASSETS — WHO IS MAKING THE MOVE?

A significant structural shift is underway in Indian household savings. The SEBI research paper documents a slow but steady movement away from traditional physical assets—gold and real estate—toward financial instruments .

The Numbers Behind the Shift

Net financial savings as a share of household savings rose from 27 percent in FY23 to 33 percent in FY25 . While physical assets still dominate the household balance sheet, the direction of change is clear.

Household savings flowing through the securities market rose from ₹2.59 lakh crore in FY23 to ₹6.91 lakh crore in FY25 . Under the revised SEBI methodology that captures secondary market transactions, SIP-driven mutual fund investments, ETFs, REITs, InvITs, and private debt placements, the true scale is even larger—₹6.91 lakh crore in FY25, nearly ₹1.5 lakh crore higher than the older estimation method would have produced .

The ₹141 Lakh Crore Stock

The revised methodology also allowed SEBI to estimate the total stock of household financial assets held through Indian securities markets—a figure never comprehensively captured before. By FY25, household assets in securities markets stood at ₹141.34 lakh crore . Equities accounted for the largest component at ₹89 lakh crore, while mutual fund holdings stood at ₹44.4 lakh crore .

This is an enormous pool of household wealth that has been built through market participation. But its distribution remains highly unequal.

The Behavioral Shift

The investing wave that picked up after COVID is now clearly visible in household savings data. The SEBI paper specifically mentions a “spectacular increase” in individual participation in markets after the pandemic . This rise coincides with the boom in investing apps, easy digital onboarding, and growing awareness around SIP investing.

But who exactly is making this shift? The data suggests that existing savers are reallocating—moving money from bank deposits to mutual funds, from gold to equities—rather than new savers entering the system. The net household secondary equity flows being negative indicates that those who are investing are also actively managing and, in many cases, exiting positions .

SECTION 3: THE NET FLOW PARADOX — NEGATIVE SECONDARY EQUITY INVESTMENTS

One of the most counterintuitive findings of the SEBI research paper concerns net household investments in the secondary equity market.

The Negative Numbers

Despite the surge in equity market participation, net household investments in the secondary equity market have remained negative for three consecutive years :

| Financial Year | Net Secondary Equity Flows (₹ Crore) |

|---|---|

| FY23 | -27,684 |

| FY24 | -69,329 |

| FY25 | -54,786 |

This means that, on aggregate, households are selling more equities in the secondary market than they are buying. They are booking profits, reallocating capital, or exiting positions .

Interpreting the Paradox

How can participation surge while net flows are negative? The answer lies in the distinction between gross and net flows. Households are both buying and selling in large volumes. The gross trading activity has increased dramatically. But when sales exceed purchases, net flows turn negative.

Jimeet Modi, Founder and CEO of SAMCO Group, offered an interpretation: “The Indian retail investor is booking gains on direct stockholdings and outsourcing fresh allocation to professional vehicles. At least in the equity cash markets, we are watching the structural shift from a punter market to an investor market unfolding in real time, on a national balance sheet” .

This shift—from direct stock trading to mutual funds—is confirmed by the primary market data. Mutual fund inflows jumped from ₹1.66 lakh crore in FY23 to nearly ₹5.13 lakh crore in FY25 .

Implications for Inequality

The negative net flow has important implications for who benefits from market expansion. If households are net sellers of equities, they are capturing gains—but also stepping away from future upside. The shift to mutual funds may provide more diversified, professionally managed exposure, but the timing of entry and exit matters enormously.

The data suggests a pattern: households buy during rallies, sell during corrections or after gains accumulate. This reactive behavior, documented across digital investor archetypes, tends to underperform a simple buy-and-hold strategy.

SECTION 4: THE DIGITAL INVESTOR ARCHETYPES — WHO ARE THE NEW PARTICIPANTS?

Digital platforms have become the fastest-growing channel for retail investing, accounting for approximately 80 percent of direct equity investors and 35 percent of mutual fund investors . The Bain “How India Invests 2025” report, using Groww’s investor base, identifies seven distinct investor archetypes that together account for roughly 75 percent of total AUM on the platform .

The Seven Archetypes

Salaried Millennials (Metro/Tier-1): The single largest block, accounting for about 20 percent of AUM. Average portfolio size: approximately ₹3.2 lakh, grown 2.6x in two years. They have the highest mutual fund share among salaried segments, lowest trading velocity, and are the most cautious—roughly one-third of portfolios sit in lower-risk mutual funds. They are emerging as the backbone of long-term, SIP-driven mutual fund flows .

Salaried Millennials (Tier-2+): Account for about 14 percent of AUM. Average portfolio: around ₹2.3 lakh, up 2.5x. Similar patterns to metro peers but with slightly higher trading activity .

Salaried Gen Z: About 10 percent of AUM. Average portfolio: around ₹1.8 lakh, expanded by roughly 2.8x. They have moved up the risk curve faster, increasing allocations to mid-cap and thematic funds. More reactive to market movements than older cohorts .

Salaried Gen X: About 10 percent of AUM. Highest average portfolio among salaried cohorts at ₹3.3 lakh, grown 2.3x. Portfolios more evenly split between direct equity and mutual funds. More measured behavior through cycles .

Self-Employed Professionals: About 12 percent of AUM. Average portfolio: ₹2.7 lakh. Balanced mix between mutual funds and direct equity. Trading activity near the middle of the pack .

Gen Z Students: About 7 percent of AUM. Smallest average portfolio at ₹0.9 lakh but fastest growth—3.1x in two years. Most responsive to market movements. Illustrates how very small starting balances translate into growth when digital access, information, and rising incomes intersect .

Business-Owner Investors: About 4 percent of AUM. Average portfolio: ₹2.6 lakh. Skewed more heavily toward direct equity. Highest trading velocity across all archetypes .

What the Archetypes Reveal

These seven archetypes demolish the notion of a single “retail investor” category. Salaried millennials in large cities with high SIP salience behave differently from Gen Z students with small portfolios and high market reactivity. Business owners with equity-heavy, high-velocity portfolios behave differently from salaried Gen X investors steadily moving toward diversified mutual funds .

The implications for inequality are significant. The archetypes that dominate AUM—salaried millennials in metros and Tier-2+ cities—are precisely those with higher education, formal employment, and urban location. The archetypes with the smallest portfolios—Gen Z students—have the fastest growth but start from a very small base. The segments that are entirely missing from this framework—rural households, informal workers, the elderly poor—are not on digital platforms at all.

SECTION 5: THE GENDER GAP — ONE-FOURTH OF PARTICIPANTS, EVEN SMALLER SHARE OF WEALTH

The gender dimension of stock market participation reveals deep structural inequalities that financial inclusion alone cannot solve.

The Participation Numbers

Women now make up one-fourth or 25 percent of market participants on the NSE . In January 2026, the growth in female investors continued consistently. States with the highest female participation include Goa (33.2 percent), Mizoram (32.5 percent), Chandigarh (32.4 percent), and Sikkim (31.4 percent) .

Maharashtra has 28.9 percent female investors—the highest among major states—followed by Gujarat at 28.3 percent . However, Uttar Pradesh, despite ranking second in overall investors, has female participation of just 19 percent—considerably below the national average of 24.9 percent .

The LXME Report’s Deeper Findings

The LXME report, produced in partnership with EY, reveals that these participation numbers mask a much more troubling reality. Women’s share of equity and mutual fund investors stands at 25 percent versus 65 percent for men—a substantial gap . Only 8.6 percent of women invest in mutual funds or equities compared to 22.3 percent of men . Only 14.2 percent of women have pensions versus 32.8 percent of men .

The report’s central argument is that financial inclusion is not financial independence. A woman may transact digitally, save diligently, and insure her family, yet remain economically fragile, asset-poor, and exposed in old age. “The binding constraint is not women’s intent or capability—it is the architecture of finance itself” .

The Four Frictions

The LXME report identifies four reinforcing frictions that sustain the gender gap :

Income Volatility: Irregular income makes long-term financial commitments feel risky, pushing women toward short-term, low-yield instruments. Over 60 percent of working women are concentrated in sectors with unpredictable earnings .

Confidence Asymmetry: Financial literacy exists without conviction. Women know more than they act on—because the system does not build belief, only knowledge.

Male-Centric Product Design: Products assume predictable incomes, linear careers, and singular decision-making—realities that match men’s lives far more than women’s.

Fragmented Journeys: Learning, saving, investing, and protection are siloed and disconnected—preventing the sequenced progression women actually need.

The Pay Gap and Retirement Gap

Women earn ₹73 for every ₹100 earned by men—a 27 percent pay gap . This translates into a 40 percent lower retirement corpus accumulated by women as compared to men .

The combination of lower earnings, lower participation in market-linked investments, and lower pension coverage creates a retirement crisis for women that is invisible in aggregate statistics. Women live longer than men but retire with less wealth—a recipe for old-age poverty.

SECTION 6: THE DARK SIDE OF THE BOOM — FINTECH PREDATORS AND FRAUDS

The rapid expansion of retail participation has attracted not only legitimate investors but also financial predators. The SEBI Chair’s warning about “finfluencers” is particularly concerning: nearly 62 percent of prospective investors are influenced by unregulated finfluencers who “present opinion as expertise and speculation as strategy” .

The Finfluencer Problem

As India’s investor base expands rapidly, the market needs more regulated advisers. But the gap is being filled by unregulated voices—on YouTube, Instagram, Telegram, and WhatsApp. These finfluencers often have no formal qualifications, no fiduciary duty to their followers, and no accountability for bad advice.

The damage is not merely theoretical. Retail investors following finfluencer tips have been caught in pump-and-dump schemes, mis-sold complex derivatives, and encouraged to take excessive risks. When losses mount, the finfluencer faces no consequences while the investor bears the full cost.

The Decline of Registered Advisers

SEBI Chair Tuhin Kanta Pandey noted a concerning trend: “It is a matter of concern that the number of registered investment advisers has declined since 2021” . As the investor base expands, the number of regulated professionals available to serve them is shrinking.

This creates a dangerous vacuum. Investors seeking guidance turn to unregulated sources because affordable, trustworthy, regulated advice is not available. The market needs more registered advisers, not fewer.

The Need for Financial Empowerment

Pandey framed the challenge as a transition from inclusion to empowerment: “India has made major progress in financial inclusion. More people today have access to bank accounts, digital payments, and investment avenues than ever before. But access alone is not enough. The next stage of India’s financial journey must be financial empowerment, which requires trustworthy advice that is unbiased, transparent, and aligned to the investor’s long-term interest” .

SECTION 7: THE BOND MARKET GAP — MISSING THE STABLE INCOME ALTERNATIVE

The stock market’s dominance in household portfolios has created an imbalance that the Economic Survey identifies as a structural vulnerability.

The Equity-Bond Imbalance

India’s equity market capitalization has surged to more than 130 percent of GDP. Meanwhile, the corporate bond market remains shallow at roughly 16–17 percent of GDP . For comparison, corporate bond markets in the United States and China account for around 40 percent and 36 percent of GDP, respectively .

This skewed structure exposes households to greater volatility while restricting the economy’s access to stable long-term funding beyond bank credit. The Economic Survey argues that developing a deep corporate bond market is critical for balanced household portfolios and long-term growth .

The Tax Distortion

The wide tax gap between equity and debt investments has distorted household allocation decisions. Long-term capital gains on equities are taxed at 12.5 percent with a ₹1.25 lakh exemption, while debt mutual funds are taxed as income at slab rates. This creates a strong incentive to favor equities even when bonds might be more appropriate for an investor’s risk profile and income needs.

The Survey calls for developing a robust debt capital market with improved transparency, enhanced price discovery, and expanded risk assessment beyond AAA-rated issuances. For households, a deeper bond market would provide access to stable, income-generating products that complement equity exposure .

Who Loses from the Bond Market Gap

The shallow bond market affects different segments of society differently. Wealthy investors can access bonds through private banking relationships. High-net-worth individuals can invest in corporate deposits and non-convertible debentures. But middle-class households lack access to retail-friendly bond products.

This matters because bond investments serve a different purpose than equities. For retirees, for those with low risk tolerance, for those seeking regular income, bonds are more appropriate than volatile stocks. The absence of a retail bond market means these investors are either forced into equities—with attendant volatility risk—or into low-yield bank deposits.

SECTION 8: THE CRIMINAL INVESTIGATION DIMENSION — WHEN MARKET GROWTH ATTRACTS SCAMS

The expansion of retail participation has also attracted criminal elements. While specific ongoing investigations cannot be detailed, the broader pattern is clear.

The Pushing-Up Phenomenon

India’s stock market frenzy has created opportunities for market manipulation. As the annual gainers list shows, some small-cap stocks have delivered returns exceeding 1,000 percent in a single year . While some of these gains reflect genuine business growth, others are driven by retail speculation and, in some cases, organized manipulation.

The Vulnerability of New Investors

New retail investors—particularly those influenced by finfluencers—are the most vulnerable to manipulation. They lack experience in distinguishing genuine opportunities from pumps, lack the resources to conduct independent research, and are more likely to chase momentum.

The result is a transfer of wealth from inexperienced retail investors to sophisticated operators—whether legitimate traders, market makers, or manipulators. The stock market boom has created winners and losers, and the losers are disproportionately the new entrants who arrived late and lack the knowledge to protect themselves.

SECTION 9: THE STRUCTURAL BARRIERS — WHY THE BOTTOM HALF STAYS OUT

Understanding who benefits from market expansion requires understanding who remains excluded. The SEBI survey’s finding that only 9.5 percent of households participate is not merely a statistic—it is a diagnostic of structural exclusion.

Income Threshold Effects

Market participation requires surplus income. For households living hand-to-mouth, investment in volatile assets is neither possible nor advisable. The bottom half of Indian households, which earns only 15 percent of national income, simply does not have the financial slack to allocate to equities.

The Formal Employment Premium

As the occupational data shows, salaried individuals have 23 percent participation—more than double the national average. This is not coincidental. Salaried employment provides predictable cash flows, formal KYC documentation, and often employer-linked access to financial products. The self-employed and informal workers lack these advantages.

Geographic Concentration of Infrastructure

The financial ecosystem—bank branches, registered advisers, mutual fund distributors—is concentrated in urban areas and developed states. A household in Nagaland or Meghalaya has far less access to financial infrastructure than a household in Delhi or Maharashtra .

Trust and Historical Experience

For older generations, particularly those who lived through the Harshad Mehta scam (1992) or the Ketan Parekh scam (2001), stock markets represent gambling, not investing. Trust in financial institutions is lower among those who have witnessed market crashes and corporate frauds.

The Missing Advisory Layer

As the SEBI Chair noted, registered investment advisers have declined even as the investor base has expanded . For a middle-class household without existing market knowledge, the absence of accessible, affordable, trustworthy advice is a binding constraint.

SECTION 10: THE CENTRAL QUESTION — BROAD-BASED WEALTH OR CONCENTRATED GAINS?

The stock market expansion of 2020-2026 represents one of the most dramatic transformations in India’s financial history. But who has truly benefited?

The Optimistic View

From one perspective, the numbers are cause for celebration. The investor base has quadrupled. Women’s participation has reached one-fourth of all investors. Tier-2+ cities are growing faster than metros. SIPs have created a systematic savings habit for millions of salaried households.

The shift from physical to financial assets is slowly unfolding. The SEBI methodology revision has revealed a much larger pool of household wealth in markets than previously understood. The post-pandemic boom has brought a new generation—millennials and Gen Z—into the investing fold.

The Critical View

From another perspective, the headline numbers obscure persistent inequality. Only 9.5 percent of households participate. The bottom 90 percent of households hold a tiny fraction of the ₹141 lakh crore in household market assets. The states with the highest participation are already the wealthiest; the poorest states remain almost entirely excluded.

Net secondary equity flows are negative, meaning households are net sellers rather than net accumulators of equity wealth. Women’s participation, while rising, remains far below men’s, and women’s retirement wealth is 40 percent lower. The bond market gap leaves middle-class households without access to stable income products.

The Unanswered Question

The central question of this topic remains unresolved: Is India’s stock market expansion building broad-based household wealth, or is it concentrating gains among the already affluent?

The answer depends on what happens next. If the current trends continue—if participation broadens to include the bottom half of households, if financial literacy translates into action, if the bond market develops to provide balanced portfolios—then the current expansion could be the foundation of broad-based wealth creation.

But if the structural barriers persist—if income inequality remains extreme, if the informal sector stays excluded, if gender gaps in income and investment continue—then the market boom will have benefited a minority while the majority watched from the sidelines.

The SEBI Chair’s framing—from inclusion to empowerment—captures the challenge. India has built the infrastructure of inclusion: bank accounts, digital payments, demat accounts, mutual fund folios. The next stage is empowerment: ensuring that this infrastructure serves all households, not just the already privileged.

As the LXME report concluded: “The binding constraint is not women’s intent or capability—it is the architecture of finance itself” . The same could be said for Indian households more broadly. The architecture of finance has been built for the salaried, urban, educated male. The next decade must redesign it for everyone else.

SUMMARY TABLE: KEY INDICATORS OF UNEQUAL MARKET PARTICIPATION

| Indicator | Value | Source | Interpretation |

|---|---|---|---|

| Households invested in securities | 9.5% (3.21 cr of 33.72 cr) | SEBI Investor Survey 2026 | 90% of households excluded |

| Awareness of securities products | 63% | SEBI Investor Survey 2026 | Awareness ≠ action |

| Mutual fund penetration | 6.7% of households | SEBI Investor Survey 2026 | Low relative to awareness |

| Direct equity penetration | 5.3% of households | SEBI Investor Survey 2026 | Even lower than MF |

| NSE registered investors | 12.7 crore | NSE, Jan 2026 | Rapid growth but multiple accounts per person |

| Household assets in securities markets | ₹141.34 lakh crore | SEBI Research Paper 2026 | Large pool but concentrated |

| Top state participation | Delhi 21%, Maharashtra 17% | SEBI Investor Survey 2026 | Wealthy states lead |

| Bottom state participation | Nagaland 3% | SEBI Investor Survey 2026 | Poor states excluded |

| Urban vs rural penetration | 23% (metros) vs 14% (small towns) | SEBI Investor Survey 2026 | Geographic concentration |

| Postgraduate penetration | 27% of households | SEBI Investor Survey 2026 | Education as predictor |

| Salaried penetration | 23% of households | SEBI Investor Survey 2026 | Formal employment premium |

| Women’s share of investors | 25% | NSE, Jan 2026 | Progress but gap remains |

| Women’s MF/equity share | 25% (vs 65% men) | LXME-EY Report 2026 | Lower participation |

| Women investing in MF/equity | 8.6% (vs 22.3% men) | LXME-EY Report 2026 | Capability not the issue |

| Net secondary equity flows (FY25) | -₹54,786 crore | SEBI Research Paper 2026 | Households net sellers |

| Corporate bond market as % of GDP | 16-17% | Economic Survey 2026 | Far below US (40%) and China (36%) |

| Financial savings share | 27% (FY23) → 33% (FY25) | SEBI Research Paper 2026 | Slow shift from physical assets |