CORPORATE LOAN WRITE-OFFS AND PUBLIC DEBATE

CORPORATE LOAN WRITE-OFFS AND PUBLIC DEBATE Examining Perceptions of Unequal Treatment Between Industries and Farmers In February 2026, Parliament was presented with a staggering set of numbers that would ignite

CORPORATE LOAN WRITE-OFFS AND PUBLIC DEBATE

Examining Perceptions of Unequal Treatment Between Industries and Farmers

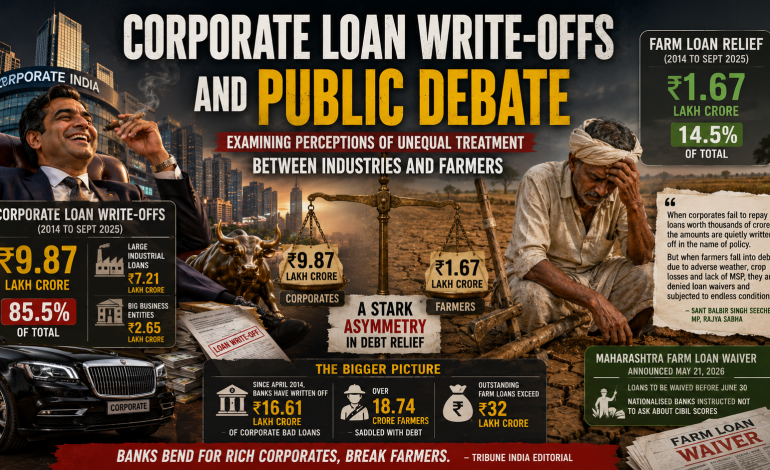

In February 2026, Parliament was presented with a staggering set of numbers that would ignite a political firestorm. Between 2014 and September 2025, the Government of India had sanctioned loan write-offs worth Rs 9.87 lakh crore to large corporate houses. During the same period, the agriculture and allied sectors received relief of merely Rs 1.67 lakh crore. In percentage terms, corporates accounted for nearly 85.5 percent of total loan write-offs, while farmers received barely 14.5 percent .

The disclosure came in response to a question raised in the Rajya Sabha by environmentalist and Member of Parliament Sant Balbir Singh Seechewal. The data showed that out of the total corporate write-offs, Rs 7.21 lakh crore pertained to large industrial loans, while more than Rs 2.65 lakh crore was written off in favour of big business entities under various banking provisions .

Reacting to the data, Seechewal offered a critique that would resonate across the political spectrum: “When the corporates fail to repay loans worth thousands of crores, the amounts are quietly written off in the name of policy. But when farmers fall into debt due to adverse weather, crop losses and the absence of Minimum Support Price, they are denied loan waivers and subjected to endless conditions” .

The asymmetry is even more pronounced when viewed over a longer timeframe. An earlier RTI response had revealed that since April 2014, banks had written off a staggering Rs 16.61 lakh crore of bad loans from corporate India. This stood in stark contrast to the plight of over 18.74 crore farmers saddled with outstanding farm loans exceeding Rs 32 lakh crore . A Tribune India editorial captured the public sentiment with biting sarcasm: “Banks bend for rich corporates, break farmers” .

Yet just three months after these national figures were laid bare, Maharashtra Chief Minister Devendra Fadnavis announced on May 21, 2026, that farmers’ loans in the state would be waived before June 30, ahead of the Kharif sowing season. Nationalised banks were instructed not to ask farmers about their CIBIL scores . The political timing was unmistakable—a direct response to opposition parties using the loan waiver issue as ammunition against the BJP-led Mahayuti government.

The contrast could not be starker. For corporations, loan write-offs are presented as a technical banking necessity—a routine “cleaning of balance sheets” to optimise capital and avail tax benefits . For farmers, every instance of debt relief is a hard-fought political battle, announced with great fanfare and tied to electoral cycles. This article examines the mechanics of loan write-offs versus waivers, the staggering scale of corporate debt relief, the political economy of farm loan waivers, and the fundamental question of unequal treatment at the heart of India’s credit architecture.

WHAT – The corporate loan write-offs versus farm loan waiver debate centres on the unequal treatment of different categories of borrowers by India’s banking system. “Write-off” refers to the accounting process by which banks remove non-performing assets from their books after making provisions, though the borrower remains legally liable for repayment . “Waiver” implies a formal forgiveness of debt, often through government intervention. The core issue is the perception that large corporate defaulters receive systematic relief through write-offs, while farmers must fight politically for every instance of debt waiver.

WHO – Key actors include the Reserve Bank of India (which regulates write-off policies and flags risks in retail lending) ; the Central Government (which disclosed the Rs 9.87 lakh crore corporate write-off figure in Parliament) ; Members of Parliament like Sant Balbir Singh Seechewal who raise these issues; State governments like Maharashtra under CM Devendra Fadnavis which announce farm loan waivers ; Banks (public and private) which execute write-offs; and the farmers and small business owners who bear the brunt of aggressive recovery while large defaulters receive concessions.

WHEN – Key data points: Rs 9.87 lakh crore corporate write-offs between 2014 and September 2025 ; Rs 10,09,511 crore written off in the last five financial years alone ; Rs 1.51 trillion expected write-offs in FY26 ; Maharashtra farm loan waiver announced May 21, 2026, effective before June 30 .

WHERE – Across India, with particular focus on industrial clusters where large corporate defaults occur, and agricultural states like Maharashtra, Punjab, Karnataka, and Rajasthan where farm distress is acute and loan waivers are politically salient.

WHY – The unequal treatment arises from multiple factors: the political economy of corporate influence (large defaulters have resources to negotiate favourable settlements); banking regulations that treat write-offs as routine balance sheet management ; the absence of a formal bankruptcy framework that treats farmers and small borrowers equitably; and the electoral salience of farm loan waivers, which makes them politically valuable announcements.

HOW – Through corporate write-offs conducted as part of banks’ “regular exercise to clean up their balance sheet, avail tax benefit and optimise capital, in accordance with RBI guidelines” . Notably, write-offs do not benefit the borrower—”borrowers of written-off loans continue to be liable for repayment” —yet in practice, recovery rates are abysmally low. Meanwhile, farm loan waivers are announced by state governments, with the state reimbursing banks for the waived amount.

SECTION 1: DEFINING THE TERMS – WRITE-OFF VS. WAIVER

The public debate around loan write-offs is often confused by the technical distinction between “write-off” and “waiver.” Understanding this distinction is essential to evaluating claims of unequal treatment.

What Is a Loan Write-Off?

According to the Reserve Bank of India, banks write off non-performing assets (NPAs) as part of their regular exercise to clean up their balance sheet, avail tax benefits, and optimise capital, in accordance with RBI guidelines and policies approved by their boards . When a loan is written off, it is removed from the bank’s balance sheet as an asset. However—and this is crucial—the borrower remains legally liable for repayment. The write-off is an accounting entry, not a forgiveness of debt .

The process works as follows: a loan becomes a non-performing asset (NPA) after 90 days of non-payment. Banks make provisions (set aside capital) against NPAs over time. When the bank concludes that recovery is unlikely or when regulatory requirements favour removal, it may write off the loan—removing it from the asset side of the balance sheet. The bank continues to pursue recovery through legal channels, but the loan no longer appears as an asset .

According to ICRA estimates, banks wrote off approximately Rs 1.37 trillion in FY25 and are expected to write off Rs 1.51 trillion in FY26 . Public sector banks are more active in writing off NPAs, especially in the final quarter of the financial year—they may remove NPAs worth over Rs 93,000 crore, while private sector counterparts may write off Rs 57,000 crore .

What Is a Loan Waiver?

A loan waiver, in contrast, is a formal forgiveness of debt. The borrower is no longer liable for repayment. When a state government announces a farm loan waiver, it typically reimburses the banks for the amount waived, so banks do not suffer losses. This is why farm loan waivers are expensive for state governments but do not directly affect bank balance sheets in the same way that corporate write-offs do.

The Critical Distinction

The distinction between write-off and waiver is technically significant but politically fraught. As Seechewal argued in Parliament, the government’s attempt to differentiate between loan write-offs and loan waivers is “misleading and designed to confuse the public” . While write-offs do not legally absolve the borrower, in practice, recovery rates from large corporate defaulters are abysmally low. A Tribune India editorial highlighted the case of Adhunik Metaliks, which settled for Rs 410 crore against outstanding dues of Rs 5,370 crore—a 92 percent “haircut” approved by the NCLT .

Seechewal’s point was simple: “When the corporates fail to repay loans worth thousands of crores, the amounts are quietly written off in the name of policy. But when farmers fall into debt due to adverse weather, crop losses and the absence of Minimum Support Price, they are denied loan waivers and subjected to endless conditions” .

SECTION 2: THE STAGGERING SCALE OF CORPORATE WRITE-OFFS

The numbers disclosed in Parliament paint a picture of systematic, large-scale relief for corporate borrowers.

The 2026 Disclosure

Between 2014 and September 30, 2025, the Central Government sanctioned loan write-offs worth Rs 9.87 lakh crore to large corporate houses. Agriculture and allied sectors received relief of only Rs 1.67 lakh crore during the same period. In percentage terms, corporates accounted for nearly 85.5 percent of total loan write-offs, while farmers received barely 14.5 percent .

Breaking this down: out of the total corporate write-offs, Rs 7.21 lakh crore pertained to large industrial loans, and more than Rs 2.65 lakh crore was written off in favour of big business entities under various banking provisions .

The Longer View: Over Rs 16 Lakh Crore

An earlier RTI response revealed even more staggering figures. Since April 1, 2014, banks have written off a staggering Rs 16.61 lakh crore of bad loans from corporate India . The Tribune India editorial noted that of the total write-off of Rs 16.61 lakh crore of toxic loans of India Inc in the past 11 years, only 16 percent was recovered. In the past five years alone, banks wrote off Rs 10.6 lakh crore of unpaid loans of India Inc, with 50 percent of the bad loans being struck off belonging to large companies .

Annual Trends

The scale of write-offs has remained consistently high. According to data presented in Parliament in March 2025, banks had written off:

-

Rs 1.61 lakh crore in 2017-18

-

Rs 2.36 lakh crore in FY19

-

Rs 2.34 lakh crore in FY20

-

Rs 2.04 lakh crore in FY21

In the last five financial years alone (as of the disclosure), banks wrote off Rs 10,09,511 crore .

The Recovery Problem

The critical issue is not the write-off itself but the abysmal recovery rates. A Tribune India editorial highlighted the case of Adhunik Metaliks, which received a 92 percent “haircut” on its dues of Rs 5,370 crore, settling for just Rs 410 crore after its resolution plan was approved by the NCLT . The editorial asked pointedly: “If the house of a Rajasthan farmer can be locked for a non-recovery of a pending amount of Rs 20,000, why couldn’t the NCLT lock the premises (and put the owners, like farmers, behind bars) of firms like Adhunik Metaliks instead of giving it a cakewalk by simply waiving 92 per cent of the pending dues?” .

Finance Minister Nirmala Sitharaman informed Parliament that write-offs do not benefit the borrower—”as borrowers of written-off loans continue to be liable for repayment and the process of recovery of dues from the borrower in written-off loan accounts continues” . Yet the experience of the Adhunik Metaliks case suggests that in practice, large corporate defaulters escape with minimal consequences.

SECTION 3: THE OTHER SIDE – FARMERS IN DEBT

While corporate write-offs are measured in lakhs of crores, the debt burden on India’s farmers is equally staggering—but without comparable relief.

The Scale of Farm Debt

According to figures cited by MP Hanuman Beniwal in Parliament, the outstanding farm loans in the country now exceed Rs 32 lakh crore. More than 18.74 crore farmers are saddled with outstanding loans . The total outstanding farm loans are 20 times higher than the outlay for the annual agricultural budget .

The Waiver Deficit

The Tribune editorial noted that while banks have consistently written off corporate loans—in the financial year 2023-24 alone, banks wrote off Rs 1.7 lakh crore, and in 2022-23, Rs 2.08 lakh crore—the Centre has done farm loan waivers only twice: in 1990 and 2008. Some state governments have done it separately, but it is not a burden on the banks as the states make the payments to the bank for the amount waived .

The Disparity in Treatment

The editorial contrasted the treatment of large defaulters with that of small borrowers:

-

A farmer from Pilibanga, Rajasthan, took a loan of Rs 2.70 lakh and had paid back Rs 2.57 lakh (including Rs 57,000 support received during the pandemic). Unable to pay back the remaining amount, he came home to find his house locked .

-

A bank in Shimoga, Karnataka, summoned a small farmer who had to walk 15 km in the absence of regular bus service to clear an outstanding balance of just Rs 3.46 .

-

A woman self-help group member was dragged to a waiting police van for her inability to pay back Rs 35,000 .

The editorial’s conclusion was damning: “It appears as if it’s only poor farmers and rural workforce that are responsible for upsetting the national balance sheet with their petty defaults, while the rich defaulters get an easy walkover” .

The Data on Farmer Suicides

Seechewal raised another critical point in Parliament: the government has stopped maintaining official data on farmer suicides, further marginalising the agrarian crisis. He had questioned the Union Agriculture Minister on farmer suicides and the denial of Minimum Support Price during the Winter Session of Parliament, receiving no satisfactory response .

SECTION 4: THE MAHARASHTRA FARM LOAN WAIVER – POLITICS AS USUAL

Against this backdrop of systemic disparity, the Maharashtra government’s announcement of a farm loan waiver on May 21, 2026, offers a case study in the political economy of debt relief.

The Announcement

Maharashtra Chief Minister Devendra Fadnavis announced that farmers’ loans in the state would be waived before June 30, 2026—ahead of the Kharif sowing season. Nationalised banks have been instructed not to ask farmers about their CIBIL scores, and an order has been given that no farmer should be hindered for any crop loan .

Fadnavis stated: “All important issues like crop loans given to farmers, waiver of farmers’ loans, availability of seeds and fertilisers for the Kharif season, as well as the rainfall forecast for the coming months were discussed. We have discussed the loan waiver with banks. There was a discussion about the format in which banks should provide information about the loan waiver, and in which format the loan waiver should be done” .

The Political Timing

The announcement came at a politically sensitive moment. Opposition parties like the Congress and the Uddhav Thackeray-led Shiv Sena had been using the farm loan waiver issue as ammunition against the Fadnavis government. The announcement could “significantly deflate the Opposition’s momentum” and benefit the BJP-led Mahayuti government by attracting farmers’ votes .

The timing—ahead of the Kharif sowing season, when farmers need credit most—was no coincidence. Farmers had demanded that loan waiver be implemented before the sowing season starts .

The Technical Details

Fadnavis directed nationalised banks to meet their target of 80 percent loan disbursement to the agriculture sector. In Maharashtra, district cooperatives and rural banks together provide 67 percent of loans, while 26 percent are provided by other nationalised banks .

The CM also noted that the El Nino effect is expected to adversely affect farmers, with only 88 percent rainfall forecast, putting more stress on the agriculture sector. His government has accelerated work on the “Jalyukta Shivar” water conservation scheme in response .

The Contrast with Corporate Relief

The Maharashtra waiver—even if implemented fully—pales in comparison to the systematic write-offs granted to corporate borrowers. A single corporate resolution (Adhunik Metaliks) received a 92 percent haircut. A single defaulter (Vijay Mallya, Nirav Modi, Mehul Choksi) owes thousands of crores. Yet each farm loan waiver is a politically hard-fought battle, announced with great fanfare, tied to electoral cycles, and subject to strict conditions.

SECTION 5: THE BANKING PERSPECTIVE – WHY WRITE-OFFS HAPPEN

To understand the disparity, one must understand the banking logic behind write-offs.

Regulatory Requirements

Banks write off NPAs as part of their regular exercise to clean up their balance sheet, avail tax benefit, and optimise capital, in accordance with RBI guidelines . The non-performing loans are taken out from books after making 100 percent provisions spread over many financial years in line with regulatory norms. Thus, the burden for setting aside money as provision does not fall in a single financial year .

The Asset Quality Review Legacy

The scale of write-offs rose substantially after the Asset Quality Review (AQR) in the second half of the last decade (2015–18 period). The AQR forced banks to recognise NPAs that had been hidden or under-reported, leading to a massive clean-up of balance sheets .

The Retail Slippage Context

Interestingly, the RBI’s latest Financial Stability Report flagged rising risks in unsecured retail lending—not corporate lending. Unsecured retail loans accounted for 53 percent of total retail loan slippages during the review period, with private sector banks contributing 76 percent of total slippages in this segment . Write-offs as a proportion of gross NPAs for private banks stood at a steep 229.7 percent .

This suggests that while corporate write-offs dominate in absolute volume, the fastest-growing stress in the banking system is actually in unsecured retail lending—personal loans, credit cards, and small-ticket consumer finance .

The Willful Defaulter Problem

Missing from the technical discussion of write-offs is the category of “willful defaulters.” The Tribune editorial noted that there are over 16,000 willful defaulters with an unpaid amount of Rs 3.45 lakh crore in bank loans, and even the RBI acknowledges these defaulters “had the money but did not want to pay back” . This is not a story of business failure or economic downturn—it is a story of deliberate non-payment by those with the capacity to pay.

SECTION 6: THE INEQUALITY ARGUMENT – BANKS BEND FOR RICH CORPORATES, BREAK FARMERS

The Tribune India editorial’s headline captured the public sentiment: “Banks bend for rich corporates, break farmers” . The argument rests on several pillars.

The Double Standard in Enforcement

Why are banking laws different for different categories of customers? Do banks ever treat those who take housing, car, tractor, or motorbike loans with the same kind of kid gloves as they treat corporate defaulters? . The editorial contrasts the aggressive recovery from a farmer with a pending amount of Rs 20,000 with the 92 percent haircut granted to a corporate defaulter with dues of Rs 5,370 crore.

The Haircut Culture

The Insolvency and Bankruptcy Code (IBC) was hailed as a transformative resolution mechanism, but recoveries for banks are coming down. The Adhunik Metaliks case—92 percent haircut—is not an isolated incident. The Tribune editorial notes that “once hailed as a transformative resolution mechanism, the IBC has come under the flap and banks are no longer enthused to use it for recoveries” .

The Question Seechewal Posed

Seechewal’s question to Parliament cut to the heart of the matter: “Does the country’s economy survive only on the corporates and not on the farmers who feed the nation?” . He reminded the House that during the COVID-19 pandemic, when industries and businesses were shut down, it was the farming sector that ensured food security and rural employment across the country .

The Dual Economic Standards

Seechewal demanded an end to what he described as “dual economic standards, where corporates receive policy protection while farmers are left to fend for themselves” . The government data on write-offs, he argued, raises “uncomfortable questions about who India’s economic policies are designed to protect—and who they leave behind” .

SECTION 7: THE WILLFUL DEFAULTER PROBLEM

No discussion of corporate loan write-offs is complete without addressing the category of willful defaulters—those who have the capacity to pay but choose not to.

The Numbers

According to the Tribune editorial, there are over 16,000 willful defaulters with an unpaid amount of Rs 3.45 lakh crore in bank loans. Even the RBI acknowledges that these defaulters “had the money but did not want to pay back” .

The Difference from Genuine Distress

A willful defaulter is fundamentally different from a borrower who has suffered genuine business failure. A company that faces market disruption, technological obsolescence, or economic downturn may legitimately be unable to repay its debts. But a willful defaulter diverts funds, creates shell companies, or simply refuses to pay while living a life of luxury.

The Missing Consequences

The editorial asked pointedly: “If the house of a Rajasthan farmer can be locked for a non-recovery of a pending amount of Rs 20,000, why couldn’t the NCLT lock the premises (and put the owners, like farmers, behind bars) of firms like Adhunik Metaliks instead of giving it cakewalk by simply waiving 92 per cent of the pending dues?” .

The answer, implicit in the question, is that the legal and banking system treats large defaulters with far greater leniency than small borrowers—not because the law says so, but because of the political and economic power that large defaulters wield.

SECTION 8: THE ECONOMIC ARGUMENT – WHY CORPORATE WRITE-OFFS ARE DEFENDED

Defenders of the current system offer several arguments for why corporate write-offs are treated differently from farm loan waivers.

The “Too Big to Fail” Argument

Large corporations employ thousands of workers, support entire supply chains, and contribute significantly to GDP. A corporate bankruptcy can trigger cascading defaults, job losses, and economic contraction. From this perspective, a 92 percent haircut for Adhunik Metaliks is not a gift to the promoters—it is a necessary sacrifice to preserve jobs and economic activity.

The Technical Necessity Argument

As Finance Minister Sitharaman noted, write-offs are a routine accounting exercise. The borrower remains liable. Banks continue to pursue recovery through legal channels. The fact that a loan appears on the balance sheet or not does not change the underlying legal obligation .

The Moral Hazard Counter-Argument

Farm loan waivers, critics argue, create moral hazard. If farmers believe their loans will be waived before every election, they have less incentive to repay. This can distort credit markets, making banks reluctant to lend to agriculture, which ultimately hurts the farmers the waivers are meant to help.

The Fiscal Constraint Argument

Corporate write-offs cost the government nothing directly—they are accounting entries on bank balance sheets. Farm loan waivers, by contrast, require state governments to reimburse banks—direct fiscal expenditure that must be budgeted. This is why the Centre has done farm loan waivers only twice in three decades.

The Counter to These Arguments

These defences, while not without merit, do not address the core grievance: the stark disparity in outcomes. Whether a corporate write-off is a technical accounting exercise or not, the borrower walks away having paid far less than owed. Whether a farm loan waiver creates moral hazard or not, the farmer facing crop failure and debt distress does not have the option of a “haircut” on his dues.

SECTION 9: THE WAY FORWARD – REFORM PROPOSALS

Addressing the perception—and reality—of unequal treatment requires structural reforms.

Strengthening Recovery from Willful Defaulters

The most glaring gap in the current system is the treatment of willful defaulters. Legal mechanisms to pursue willful defaulters—including asset seizure, travel bans, and criminal prosecution—exist but are underutilised. The Tribunal editorial’s question about why the NCLT cannot treat defaulters like Adhunik Metaliks the same way banks treat a farmer with a Rs 20,000 default is not rhetorical—it deserves an answer .

Institutionalised Farm Debt Relief

Instead of ad hoc, election-driven farm loan waivers, India needs an institutional mechanism for farm debt relief linked to verifiable distress—crop failure, weather events, price collapses. This would remove the political uncertainty around farm debt relief while ensuring that genuinely distressed farmers receive support.

Transparency in Write-Offs

Banks should be required to disclose, for each write-off above a certain threshold, the identity of the borrower, the amount written off, the recovery expected, and the rationale. While privacy concerns exist for individual borrowers, corporate write-offs involve public money through government-owned banks and deserve public scrutiny.

The Inevitability of the Question

The Tribune editorial ended with a question that remains unanswered: “If such a massive ‘haircut’ is required for a big company, why shouldn’t farmers get the benefit of a similar approach and, that too, in a relatively smaller way? After all, their individual outstanding loans are hardly a fraction of the corporate bad debts” .

SECTION 10: THE CENTRAL QUESTION – WHOSE DEBT MATTERS?

The politics of corporate loan write-offs and farm loan waivers reflects a fundamental tension in India’s economic governance: whose debt is treated as a systemic problem requiring collective solution, and whose debt is treated as individual failure requiring punishment?

Two Worlds of Debt

In the world of corporate debt, default is treated as a technical problem. Banks write off loans, the IBC facilitates haircuts, and promoters walk away to start new ventures. The language is technocratic: “balance sheet cleaning,” “capital optimisation,” “resolution mechanism.”

In the world of farm debt, default is treated as a moral failing. Farmers face aggressive recovery, seizure of assets, and—in the most extreme cases—suicide. The language is judgmental: “default,” “willful,” “responsible for upsetting the national balance sheet” .

The Data That Cannot Be Ignored

The government’s own data shows that between 2014 and September 2025, corporates received Rs 9.87 lakh crore in write-offs while farmers received Rs 1.67 lakh crore . The longer-term figure of Rs 16.61 lakh crore since 2014 makes the disparity even starker .

The Unanswered Question

The central question of this topic remains unresolved: Why does the Indian banking system treat the debts of large corporations as a collective problem requiring systemic solutions, while treating the debts of farmers as individual failures requiring punitive recovery?

Seechewal’s question to Parliament echoes: “Does the country’s economy survive only on the corporates and not on the farmers who feed the nation?” .

The Maharashtra farm loan waiver of May 2026 is a reminder that when farmers organize politically, they can secure relief. But the contrast with the systematic, routine, and largely invisible write-offs granted to corporate borrowers could not be starker.

As the Tribune editorial concluded: “It appears as if it’s only poor farmers and rural workforce that are responsible for upsetting the national balance sheet with their petty defaults, while the rich defaulters get an easy walkover” .

Until the banking system addresses this perception—and the reality that underlies it—the debate over unequal treatment will continue to fuel public anger and political mobilization.

SUMMARY TABLE: CORPORATE WRITE-OFFS VS. FARM RELIEF

| Indicator | Corporate | Agriculture | Source |

|---|---|---|---|

| Loan write-offs/relief (2014-Sept 2025) | Rs 9.87 lakh crore (85.5%) | Rs 1.67 lakh crore (14.5%) | Indian Express/Parliament |

| Long-term write-offs (since April 2014) | Rs 16.61 lakh crore | Not separately quantified | Tribune India/RTI |

| Outstanding debt burden | Part of corporate NPA figures | Rs 32+ lakh crore (18.74 cr farmers) | Tribune India/Parliament |

| Willful defaulters | 16,000+ defaulters, Rs 3.45 lakh crore | Not applicable | Tribune India |

| Write-offs FY18 | Rs 1.61 lakh crore | Minimal | Business Standard |

| Write-offs FY19 | Rs 2.36 lakh crore | Minimal | Business Standard |

| Write-offs FY20 | Rs 2.34 lakh crore | Minimal | Business Standard |

| Write-offs FY21 | Rs 2.04 lakh crore | Minimal | Business Standard |

| Write-offs last 5 years | Rs 10,09,511 crore | Minimal | Business Standard/Parliament |

| Expected write-offs FY26 | Rs 1.51 lakh crore | Minimal | ICRA/Business Standard |

| Recent farm relief | N/A | Maharashtra waiver (May 2026) | UNI/The Statesman |